Nickel Mines LTD.

Nickel surged by the 15% exchange limit for a second day in London, putting the spotlight back on bearish position holders just two weeks since the market was roiled by an historic short squeeze.

The move reduces the size of the potential pain for Xiang and his banks as prices are on the march again. However, the businessman and his allies have only reduced a portion of their total short position, and still hold large bets on falling prices, the people said.

“Ultimately the short position is still out there, and they will have to close it out,” Michael Widmer, head of metals research at Bank of America Corp., said by phone from London. Sharp daily price moves are likely to continue “at least until the short position is out of the market.”

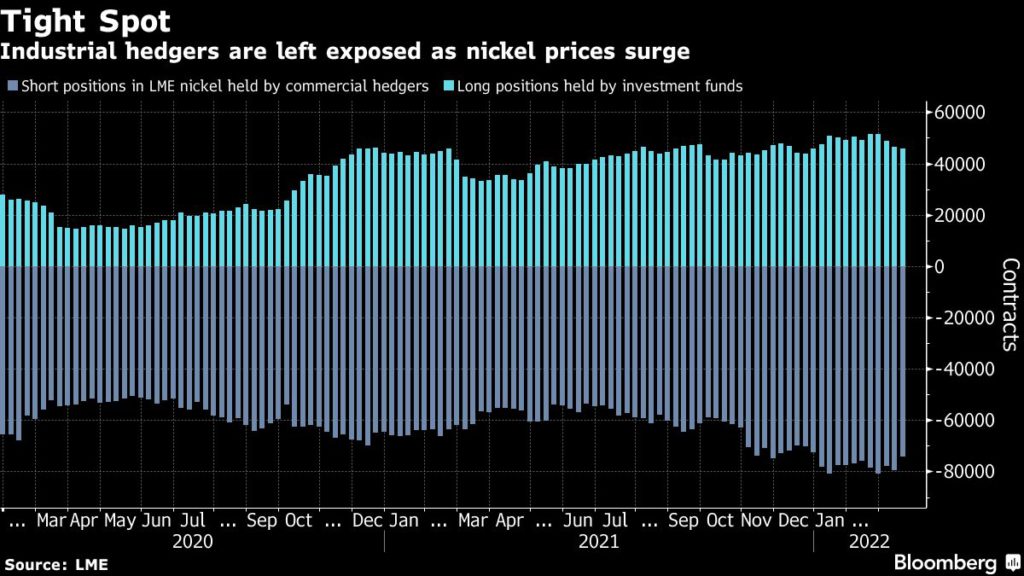

While Tsingshan holds an outsized short position on the LME, there are many other industrial users and physical traders who hold short positions to hedge their price risk, raising the threat of another squeeze if those parties need to buy their positions back, or brokers seek to close them out to avoid further margin calls.

The total risk-reducing short positions held by commercial parties stood at 74,166 contracts at the end of last week, according to data from the bourse. To a large extent, they’ll need to turn to bullish hedge funds to liquidate their contracts — on a net basis investment funds are the largest holders of long positions in the LME nickel market.

To be sure, even if short position holders come under pressure, the new daily price limits introduced by the LME will help prevent a repeat of the extreme price swings seen earlier this month.

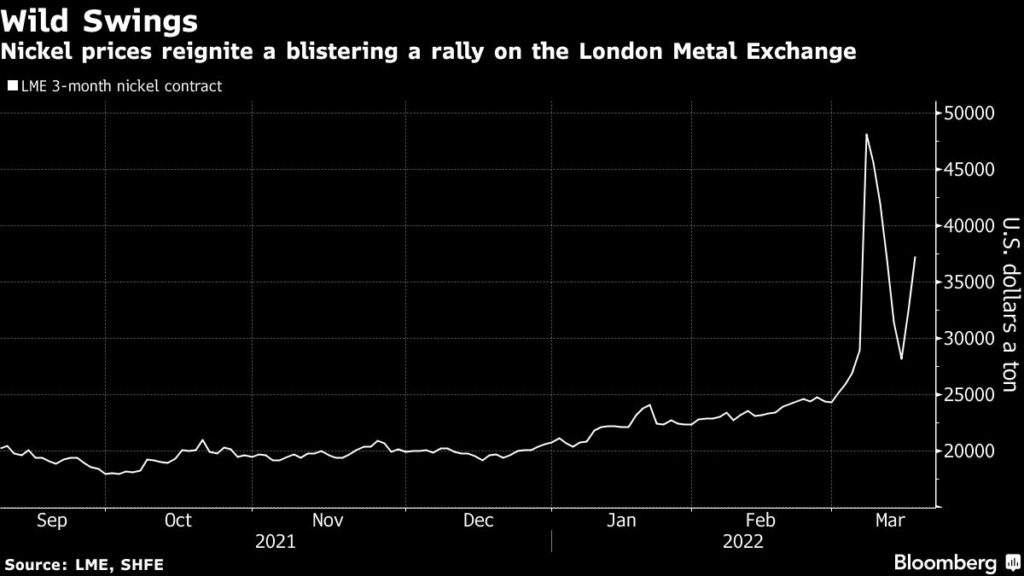

When nickel prices spiked in early March, the LME intervened to suspend buying and selling and canceled billions of dollars of deals in a move that drew furious criticism from many traders and investors. The market plunged when it reopened, and is now down about 63% from the record high, but up 53% so far this month. Prices rose to $37,235 a ton on Thursday.

The latest surge comes after trading had only just restarted in earnest this week, with lower prices drawing in buyers following four days of limit-down moves when the market reopened from the week-long suspension.

Shanghai Futures Exchange nickel contracts also initially surged to the maximum daily limit as the evening session got underway, tracking gains in London. Prices then moderated, and were trading 4.9% higher at 257,660 yuan ($40,463) a ton as of 3:20 p.m. London time. That equates to about $35,800 a ton when VAT is deducted.

Trading is becoming increasingly illiquid on the LME, with many investors looking to liquidate their positions in the wake of nickel’s unprecedented volatility.

Roiling price moves are also sparking turmoil in broader commodities markets and some of the world’s top physical traders warned that eye-watering margin calls are forcing them to reduce their activity, driving liquidity out of markets and exacerbating price swings.

(By Mark Burton and Jack Farchy)

No comments:

Post a Comment