Singapore (Platts)--28 Nov 2017 1000 pm EST/300 GMT

China's crude oil imports from the US in October

surged 77.3% month on month to average of 208,000 b/d, or a total of

878,623 mt, making the US the country's ninth top crude supplier, data

released Monday by China's General Administration of Customs showed.

In the same month last year, no US crude oil imports were recorded.

The

US inflow in October was likely due to buying from state-owned

refiners, as arrivals for independent refiners was down 42% from

September at 163,000 mt, an S&P Global Platts survey showed.

Unipec had been actively offered US crude, according to state-owned Sinopec.

Unipec is the international trading arm of Asia's biggest refiner, China

Petroleum and Chemical Corp., or Sinopec. Sinopec's Qilu refinery in

October received its first cargo of US crude, a cargo of Mars crude.

China's

total crude oil imports fell to a 12-month low of 31.03 million mt

(7.34 million b/d) in October, down 18.9% from September. China's crude

imports typically fall in October.

Russia remained China's top crude supplier in October, though shipments fell 26.8% month on month to 4.65 million mt.

Saudi

Arabia climbed to the second place in October from third in the

previous month and was the only supplier among the top three to register

a month-on-month increase.

US MARKET SHARE TO GROW

China's crude imports from the US are expected to grow next year, according to trade sources.

In

the first 10 months of 2017, China's imports from North America surged

to 150,000 b/d, or 6.22 million mt, from just 15,500 b/d a year ago, led

by higher volumes from the United States .

This expanded the region's market share in China to 1.8%, from 0.2% in the same period last year.

Unipec

is forecast to double its imports from the US in 2018 to 200,000 b/d,

but expects China's total crude imports to grow at less than 5% next

year, the company's general manager Chen Bo said last week at the China

International Oil and Gas Trade Congress in Shanghai .

China

imported 8.42 million b/d of crude oil in the first 10 months of this

year, up 12.2% year on year, the latest data from the General

Administration of Customs showed.

The market share of OPEC

members fell to 55.1% in the January-October period from 57.9%, while

Middle Eastern producers also saw their market share falling to 43.3%

from 48.4%. But Africa's market share rose by two percentage points from

last year to 20%.

U.S. oil prices fell more than 1 percent on Monday,

easing from two-year highs on prospects of higher supply from a planned

restart of the Keystone crude pipeline and uncertainty about Russia’s

resolve to join in extending output cuts ahead of this week’s OPEC

meeting.

FILE

PHOTO: Equipment used to process carbon dioxide, crude oil and water is

seen at an Occidental Petroleum Corp enhanced oil recovery project in

Hobbs, New Mexico, U.S. on May 3, 2017. Picture taken on May 3, 2017.

REUTERS/Ernest Scheyder/File Photo

TransCanada Corp (TRP.TO)

said it will restart its Keystone crude oil pipeline at reduced

pressure on Tuesday after getting approval from U.S. regulators.

Calgary-based

TransCanada shut down the 590,000 barrel-per-day pipeline, one of

Canada’s main crude export routes to the United States, on Nov. 16 after

5,000 barrels of oil leaked in South Dakota. Keystone carries crude

from Alberta’s oil sands to U.S. refineries.

Brent

futures LCOc1 ended down just 2 cents at $63.84 a barrel while U.S.

crude CLc1 settled 84 cents, or 1.4 percent, lower at $58.11 a barrel.

On Friday, U.S. crude touched $59.05 a barrel, its strongest since mid-2015, following the spill.

In

post-settlement trading the front month spread for U.S. crude spread

hit a session low of negative 10 cents a barrel, after Transcanada’s

restart announcement.

Oil prices have surged in

recent months due to output cuts by the Organization of the Petroleum

Exporting Countries, Russia and other producers. However, higher prices

have encouraged greater output among U.S. producers.

OPEC

and its allies cut production by 1.8 million bpd in January and have

agreed to hold down output until March. OPEC meets on Thursday to

discuss policy and most analysts expect a deal to extend the cuts.

On

Friday, Russia said it was ready to support extending an output cut

deal. Still, Russia has not given a timeline, and on Monday there were

signs Russia may find it hard to comply.

Oil

output from Russia’s Sakhalin-1 project is set to rise by about a

quarter to 250,000-260,000 barrels per day (bpd) from January, sources

with knowledge of the plan said.

“It’s the OPEC

parlor game that we’re all playing,” said John Kilduff, partner at

Again Capital LLC in New York, “The Russians being quiet about their

intentions about the OPEC deal is a little unsettling.”

Oil

markets will rebalance after June 2018 at the earliest, an OPEC working

panel concluded last week, OPEC sources said on Monday, signaling the

need to extend existing production cuts well into next year.

Analysts

at Barclays expect OPEC to keep output limits for another six or nine

months. However, they said this was widely expected, so prices still

might fall after the OPEC meeting.

Harry Tchilinguirian, head of oil strategy at French bank BNP Paribas, also saw “plenty of room for disappointment.”

“Should

the outcome of the next OPEC meeting fall short of expectations, the

large net-long speculative position on oil futures can unwind, sending

prices lower and volatility higher.”

Additional

reporting by Christopher Johnson in London, Henning Gloystein in

Singapore; Editing by David Gregorio, Edmund Blair and Mark Potter

During

President Donald Trump’s visit to Asia this week, a Chinese energy

company pledged to spend almost $84 billion helping West Virginia build

an entire supply chain that would bring the benefits of America’s shale

gas boom to bear.

Much of it will probably never materialize. Here are the reasons why.

Storage Hub

In July, Senator Joe Manchin, a West Virginia Democrat,

joined other policy makers to pitch a $10 billion Appalachian storage

hub to Trump. The proposal outlined underground storage in Pennsylvania, Ohio and West Virginia,

plus pipeline to link storage and petrochemical plants. A report from

the American Chemistry Council found that, if approved, it could create

more than 100,000 jobs and nearly $36 billion in capital investment.

As shipping gas southeast becomes more expensive, any opportunity to

store gas locally may stoke desire for the cheaper fuel there, said

Stephen Schork, president of Schork Group Inc., a gas industry

consultant in Villanova, Pennsylvania.

"It would be more than competitive," Schork said. "The price of natural gas in the Marcellus shale is really advantageous."

And the MOU with China Energy Investment may be one step toward that.

According to the West Virginia Department of Commerce, the company has

already made “several trips” to the state. On Thursday, Governor Jim Justice described the agreement as proof that “the tides are turning in West Virginia.”

The Returns

China Energy Investment Corp. and West Virginia have grand

-- albeit non-binding -- plans to build new gas-fired power plants,

along with complexes to store the fuel and chemical plants to help turn

it into plastics. Based on a statement from West Virginia’s Department

of Commerce, China Energy Investment would spend $83.7 billion over 20

years, or more than $4 billion annually.

China Energy Investment was formed from the combination of Shenhua

Group Corp., the nation’s largest coal miner, and China Guodian Corp.,

one of its top-five power generators, making the combined power company

the world’s biggest.

As Bloomberg Intelligence energy analyst Michael Kay points out, not

even U.S. energy pipeline giant Kinder Morgan Inc. budgets that much for

growth projects. There just isn’t enough infrastructure with high

enough returns to make it worthwhile.

“That’s not going to happen,” Kay says. “The problem isn’t necessarily anything other than financial.”

On the surface, a massive build-out of infrastructure in Appalachia

-- a region that now supplies more than a third of America’s natural gas

-- makes sense.

Companies and politicians have been pushing for more pipelines and

plants there since the shale boom unleashed a flood of gas from

formations like the Marcellus a decade ago. West Virginia, in the heart

of Coal Country, could especially use the help after a market collapse

forced shut hundreds of U.S. mines. Another plus -- the region offers an

alternative to the hurricane-prone Gulf Coast.

The Rival

One reason more projects haven’t taken off: The Gulf Coast

is an easier and often cheaper alternative with existing pipelines to

power plants, chemical plants and storage tanks. Meanwhile Texas is home

to its own giant shale plays, including the Permian Basin where 9

billion cubic feet of gas is pulled from oil wells every day.

“When you already have a market established in the Gulf Coast,

it’s easy to expand it -- you have a lot of storage, you have a lot of

supply,” said Prachi Mehta, a natural gas liquids analyst for Wood Mackenzie Ltd. In Appalachia, “you have a lot of constraints.”

The Opposition

But by far the biggest constraint that energy companies face in the eastern U.S. is the regulatory process.

Some project developers have spent over a year waiting for federal

approval as landowners and environmentalists there lodge complaints and

stage protests. Even as politicians push for more investments, pipeline

giants from Energy Transfer Partners LP to Williams Partners LP are

being forced to delay projects because of regulatory setbacks and legal

challenges.

Even Dave Spigelmyer, president of a coalition that’s been pushing

for the kinds of projects China Energy Investment has pledged to build,

acknowledges the challenges.

"We need to make sure we have our A-game on, because folks are going to go where they have certainty on the return on investment,” Spigelmyer said. “When you talk about investment in Pennsylvania, it takes over 100 days to get a drilling permit.”

The Money Spent

Another reason West Virginia shouldn’t get its hopes up,

Kay said, is the fact that much of the major investments that

Appalachia’s energy market needs may have already been made.

Enough pipelines are coming online to increase the region’s

take-away capacity by about a third. And so much gas-fired power

generation has been built in the area that Moody’s Investors Service has

warned of “a gas-driven apocalypse” in the power market.

Later this year, Dominion Energy Inc. will bring online a liquefied

natural gas export terminal in Maryland, and an ethane export terminal

at Marcus Hook, Pennsylvania, is already sending cargoes overseas.

“The truth is,” Kay said, “we need to see these projects coming online to see if we do need more infrastructure.”

To be sure, a record volume of gas keeps flowing out of the Marcellus

and Utica shale formations of the eastern U.S. IHS Markit forecasts

that, between 2026 and 2030, the region will produce enough natural-gas

liquids to supply as many as four more chemical plants that “crack” the

ethane in natural gas streams into a chemical widely used by

manufacturers.

A

commissioner from Mexico's energy regulatory commission (CRE) said

technical challenges and a highly complex environment were to blame for

months of delay in the opening up of state-run Pemex's fuel

infrastructure.

The CRE is in charge of opening up Pemex's existing fuel transport and storage infrastructure to third parties through a program of gradual and regional open seasons.

US independent refiner Andeavor, formally known as Tesoro, won capacity in Pemex's first open season in the northwestern states of Baja California and Sonora in May.

But subsequent open seasons have been suspended indefinitely, and are now several months behind schedule.

"The first open season was fairly straightforward, with little operative complexity,"

CRE commissioner Montserrat Ramiro Ximenez said this week. But

commissioners have found the second open season for all other northern

border states particularly challenging.

Many pipelines arrive directly inside Pemex's refinery, Ramiro said,

requiring permits that were not under the authority of the CRE and

causing further delays.

Whether the capacity volume Pemex wanted to offer

was big enough to make the open season viable was another thorny issue,

with an operator reluctant to abandon its infrastructure on one side,

and new participants eager to acquire capacity on the other.

"The open season presupposes that Pemex has enough capacity for

others to transport their fuel, but in many cases, we [Pemex and the

CRE] have conflicting opinions about what can be made available or not," Ramiro said. "Logistics in Mexico is a very complicated cocktail."

Ramiro was answering other panelists at the Mexico International

Energy conference, who echoed some of the main worries in the industry.

Since independent fuel imports were allowed in April 2016, as a result

of a groundbreaking energy reform, they have remained fairly low.

In October, the latest available data, independent gasoline were

growing but still only accounted for 0.8pc of all gasoline imports that

month, at 147,800 bl (or 4,764 b/d).

"When it comes to logistics, we are in total darkness," a former manager of Pemex fuel retail stations, Juan Lopez Huesca, said on the same panel. "Without the opening of the owner's infrastructure it cannot work."

Carlos Rodriguez, operations manager at Bulk Shipping Mexico, a

company that moves products, said a number of potential clients had

approached him to export fuel to Mexico.

"They want to bring product to Mexico, but we have nowhere to put it, it all belongs to Pemex," Rodriguez said.

Both argued that postponing the open seasons without clear

explanations since May has sent a red flag to investors. While new

projects for fuel storage terminals are underway, investment in new

pipelines remain scarce.

Ramiro acknowledged that the CRE had to fix the open season delay and

send a positive signal to the industry. But the commissioner argued

that investors need not wait for the open season to invest in

infrastructure.

"It became clear that we need more infrastructure, that Pemex's

infrastructure is insufficient and that, on top of that, it is very

complex to try and share with somebody who does not want to lose its

market and that has not separated its logistics arm from its refinery

arm," Ramiro said. "It is easy to make a viable case for new infrastructure."

Saudi authorities are striking agreements with some of those held in an alleged anti-corruption crackdown, asking them to hand over assets and cash in return for their freedom, according to sources familiar with the matter.

The deals involve separating cash from assets, such as property and

shares, and looking at bank accounts to assess cash values, one of the

sources told the Reuters news agency.

Dozens of princes, senior officials and businessmen, including

cabinet ministers and billionaires, have been arrested in this month's

sweeping crackdown, which is being seen as an attempt to strengthen the

power of Crown Prince Mohammed bin Salman.

Among those arrested was billionaire Prince Alwaleed bin Talal, one of the kingdom's most prominent businessmen.

One businessman reportedly had tens of millions of Saudi

riyals withdrawn from his account after he signed the deal. In another

case, a former senior official consented to hand over ownership of four

billion riyals (roughly $1.06bn) worth of shares, the source said.

The Saudi government earlier this week moved from

freezing accounts to issuing instructions for "expropriation of

unencumbered assets" or seizure of assets, said a second source familiar

with the situation.

There was no immediate comment from the Saudi government on the

deals, and the sources declined to be identified because the agreements

are not public.

Analysts say the deals could help to end uncertainty about the

crackdown, but they could also have an affect on Saudi Arabia's risk

perception among investors.

"Eliminating uncertainty about what the Saudi authorities are going

to do goes a long way towards giving the market comfort that the regime

is getting its house in order and plugging its deficit," said Louis

Gargour, founder and senior portfolio manager at the London-based hedge

fund LNG Capital.

Riyadh has been cutting spending while raising taxes and fees to curb

a state budget deficit caused by low oil prices. The deficit, which hit

$98bn in 2015, is shrinking, but at a high cost to the economy; data in

late September showed Saudi Arabia in recession during the second

quarter.

The Saudi government has in recent years been pressing wealthy

individuals to invest more in the kingdom and bring home some of their

wealth from overseas.

Washington monitoring situation

The United States is closely watching the situation in Saudi Arabia, US Treasury Secretary Steven Mnuchin said on Friday.

Asked about agreements to hand over wealth for detainees' freedom,

Mnuchin told CNBC: "I think that the Crown Prince [Mohammed bin Salman]

is doing a great job at transforming the country."

According to Gargour, "from a civil liberties point of view,

obviously incarcerating people doesn't give us comfort, and that's why

we've seen spreads on Saudi bonds go 50 basis points or so wider".

Funds started selling Middle East bonds early this month after Saudi

Arabia arrested dozens of senior officials and businessmen in an

unprecedented crackdown, which the government said was aimed at tackling

corruption.

Credit spreads and the cost of insuring debt against default have

increased not only for Saudi Arabia and Lebanon, but across the

six-nation Gulf Cooperation Council, which includes Qatar, Kuwait and

Abu Dhabi.

"From a trading point of view, you want to identify the private

companies most impacted and short or sell them, and conversely public

sector companies will benefit," Gargour said.

The market value of the portfolio of Saudi equities held by the

Public Investment Fund, the kingdom's sovereign wealth fund, has gained,

even as the arrest or questioning of more than 200 people in the

inquiry caused stocks in many privately controlled firms to slump.

Reuters could not immediately verify a Financial Times report stating

that in some cases, the government is seeking to appropriate as much as

70 percent of suspects' wealth to channel hundreds of billions of

dollars into depleted state coffers.

Saudi authorities have help from international auditors,

investigators and people with experience in tracing assets. Bank

representatives are on hand to execute the decisions immediately, one of

the sources said.

Hundreds held

Saudi authorities said they have questioned 208 people in an

anti-corruption investigation and estimate that at least $100bn has been

stolen through fraud, an official said last week, as the inquiry

expanded beyond the kingdom's borders into the United Arab Emirates.

Those held include other high-profile businessmen, such as Mohammad

al-Amoudi, whose wealth is estimated by Forbes at $10.4bn, with

construction, agriculture and energy companies in Sweden, Saudi Arabia

and Ethiopia; and finance and healthcare magnate Saleh Kamel, whose

fortune is estimated at $2.3bn.

Crown Prince Mohammed bin Salman is trying to use the purge as a way

of boosting his popularity with the Saudi population, said Jason Tuvey, a

Middle East economist at Capital Economics.

"But he may have realised that by doing this, he's gone a step too

far and ruffled too many feathers, and he is maybe trying to find a way

out that means these people don't end up in prison forever and can carry

on their business operations as before."

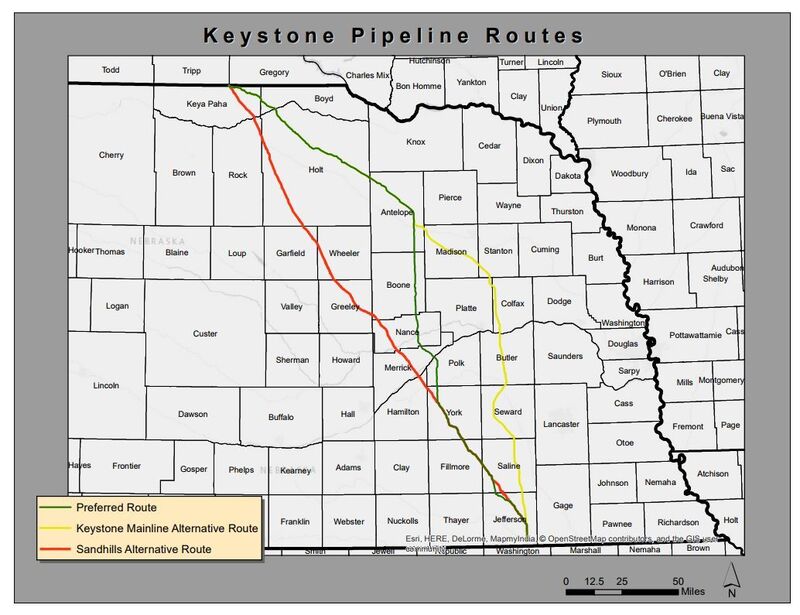

Nebraska’s approval of an alternative route could throw more

uncertainty into the mix for the long-delayed Keystone XL oil pipeline.

The Public Service Commission approved TransCanada Corp.’s

project on a three-to-two vote, removing one of the last hurdles to the

Calgary-based company’s construction of the $8 billion, 1,179-mile

(1,897-kilometer) conduit, which has been on its drawing boards since

2008. The decision, though, wasn’t wrinkle-free: The panel mandated an

alternative route that was immediately targeted by the project’s

opponents as lacking adequate vetting.

TransCanada

is now "assessing how the decision would impact the cost and schedule

of the project,” Russ Girling, TransCanada’s chief executive officer,

said in a statement. The company’s shares rose 1.3 percent to C$63.35 at

12:24 p.m. in New York trading.

Source: Nebraska Public Service Commission

The uncertainty expressed by Girling was quickly reflected in analyst notes.

"While

today’s Keystone XL pipeline approval is an important milestone, it

does not provide certainty that the project will ultimately be built and

begin operating," said Gavin MacFarlane, a vice president at Moody’s

Investors Service. “Pipeline construction would negatively affect

TransCanada’s business risk profile through increased project execution

risk, and would likely put pressure on financial metrics."

Jane

Kleeb, president of the environmental advocacy group Bold Alliance, said

green-lighting the alternative may have helped the commission reach a

"middle ground solution.” But it opens new questions that she said her

group would likely explore in federal court.

That view mirrored a

dissenting opinion from Commissioner Crystal Rhoades. The alternative

route needed more study on both the state and federal level, she

said before the final vote, and it failed to give landowners along that

different path the ability to address the commission.

The

commissioners who supported the route change said it would impact fewer

threatened and endangered species, fewer wells, less irrigated cropland,

and that it included one less river crossing.

Additionally, they wrote, “it is in the public interest for

the pipelines to be in closer proximity to each other, so as to maximize

monitoring resources and increase the efficiency of response times”

with “issues that may arise with either pipeline.”

South Dakota Spill

The

decision came just days after a spill on TransCanada’s existing

Keystone line in South Dakota on Thursday sparked new attacks by

environmentalists who pointed to the event as something the state could

expect if the project is approved.

In its post-hearing brief,

TransCanada told the panel its "preferred route was the product of

literally years of study, analysis and refinement by Keystone, federal

agencies and Nebraska agencies," and that no alternate route, even one

paralleling the Keystone mainline as the approved path does, was truly

comparable.

Demonstrators hold a rally against the Keystone XL pipeline outside of the White House on Jan. 10, 2015.

Photographer: Pete Marovich/Bloomberg

Producers

in the Alberta oil sands region and elsewhere in Western Canada are

facing pipeline bottlenecks, forcing increased volumes onto rail cars.

Since rail is a more expensive form of transport, heavy Canadian crude

prices will need to trade at a bigger discount to West Texas

Intermediate futures.

That discount widened to more than $15 a

barrel Monday from less than $10 in August. Keystone XL construction,

along with Kinder Morgan Inc.’s Trans Mountain expansion and Enbridge

Inc.’s Line 3 expansion, could narrow the gap to less than $10 by early

next decade, Tim Pickering, chief investment officer at Auspice Capital

Advisors Ltd., said in a telephone interview.

Mexico, Venezuela

The

pipeline may also be more commercially viable given declining heavy oil

production in Mexico and ongoing instability in Venezuela, said Zachary

Rogers, a refining and oil markets research analyst at Wood Mackenzie,

said in a statement. Canadian producers are an alternate source of heavy

crude for U.S. Gulf Coast refiners.

Brett Harris, a spokesman for Calgary-based Cenovus Energy Inc.,

a committed oil-sands shipper on the proposed pipeline, said the

approval “is in the best interest of the industry, best interest of

Canada and the best interest of the U.S. as well. We are pleased to see

that decision.”

Dennis McConaghy, former executive vice president

of corporate development at TransCanada, said he would expect senior

management to announce they will go ahead with the project by year’s end

with construction by the later half of 2019. Completion of the line

would come a couple years later.

“The project could have been very seriously set back if they hadn’t got this approval today,” he said.

Volume Needed

McConaghy

said he believes the company has secured the volume needed to make the

project economically viable. But he added that “there is no question

there is going to be all kinds of legal obstruction that will be

resorted to by opponents.”

Nebraska’s decision overrode the

objections of environmental groups, Native American tribes and

landowners along the pipeline’s prospective route. The project had the

support of the state’s governor, Republican Pete Ricketts, its chamber

of commerce, trade unions and the petroleum industry.

With

Nebraska’s go-ahead in hand, TransCanada still must formally decide

whether to proceed with construction on the line, which would send crude

from Hardisty, Alberta, through Montana and South Dakota to Nebraska,

where it will connect to pipelines leading to U.S. Gulf Coast

refineries. The XL pipeline would add the ability to move 830,000

barrels a day, more than doubling the existing line’s capacity.

Shipping Commitments

The

company’s open season for gauging producers’ interest closed late last

month, and TransCanada executives have indicated that they’ve secured enough shipping commitments to make the project commercially worthwhile.

President Barack Obama’s administration rejected the pipeline in 2015. President Donald Trump

vowed to reverse that determination and, in January, invited the

company to reapply. Approval was quickly granted. He also championed

completion of the Energy Transfer Partners LP-led Dakota Access Pipeline, which runs from northwestern North Dakota to Illinois via South Dakota and Iowa.

The

panel heard testimony and took in evidence during a four-day August

hearing. Its power over the project is drawn from the state’s

constitution.

The case is In the Matter of the Application of TransCanada Keystone Pipeline LP for Route Approval of the Keystone XL Pipeline Project, 0p-0003, Nebraska Public Service Commission (Lincoln).

November’s VLCC Meg programme was concluded last week with some 132 cargoes fixed, volumes not seen since January.

We are currently between months and as usual activity is a bit subdued, Fearnleys said in its weekly report.

A couple of December deals were done, but basically BOT cargoes and rates were concluded at last done levels.

Saudi stem-confirmations could possibly be out by the end of this week.

WAfrica/East activity was also a bit slower, but owners were resilient

and rates remained stable, as optimism was still in place for the

winter.

Suezmaxes experienced steadily eroding rates over the past week, with

WAfrica slipping from the low WS80’s down to WS72.5 for TD20. End

November cargoes were thin on the ground and other areas remained quiet

allowing tonnage to build up.

Owners earnings were further eaten into by increasingly expensive

bunkers adding to the pain. The earnings are now below the $10,000 per

day threshold.

Thus far, the Turkish Straits delays have been unseasonably minimal,

although this is expected to change in the weeks ahead of the winter

months.

There is a glimmer of hope in the Med and Black Sea, where there was a

sudden flurry of action with Aframaxes and lists tightened. This was the

trigger a year ago for Suezmaxes and owners will be watching with keen

interest for any opportunity to capitalise.

The week ahead has a softer feel but this could turn around on

increased volume or weather delays. Norwegian meteorologists are

guessing that there will be a warm start to this winter season, and

North Sea and Baltic Aframax markets should be moving sideways heading

towards December.

The fact that there is a five- day maintenance period coming up at Primorsk undermines the ’bold’ statement above.

The Med and Black Sea softened last week and has remained rather flat

ever since. However, it is looking to firm up next week again, as

tonnage is quickly being picked up for early 1st decade, leaving the

cross-Med cargoes with fewer options going forward, Fearnleys concluded.

Crude tanker freight rates are expected to decline further next year,

following a sharp decline in 2017, according to the latest edition of

the Tanker Forecaster, published by shipping consultancy Drewry.

Although crude tonnage supply growth is expected to be low next year

after surging in 2017, this will not be enough to push tonnage

utilisation rates higher, as demand growth is expected to be sluggish. A

slowdown in global oil demand growth and a likely decline in China’s

stocking activity will keep growth in the crude oil trade moderate next

year.

After a sharp decline in 2016, freight rates in the crude tanker market

have declined further this year, despite strong tonnage demand growth

in the two years, thanks to a surge in tonnage supply.

Fleet growth is expected to come down to 3.2% in 2018, after increasing

by close to 6% per year in 2016 and 2017. However, this is unlikely to

provide any respite to owners, as rates will continue to decline in 2018

on account of a slowdown in crude oil trade growth. Global oil demand

growth is expected to fall to 1.4 mill per day in 2018 from 1.6 mill per

day in 2017, Drewry said.

In addition, a likely slowdown in China’s stocking activity poses a big

risk to crude tonnage demand. This activity, which remained one of the

leading factors behind the strong growth in the crude oil trade over the

last two years, may fall significantly in 2018.

According to the IEA’s data on China’s implied stock changes, the

country should have accumulated close to 520 mill barrels since 2015,

well above the total special petroleum reserve (SPR) capacity that was

supposed to come online fully by 2020.

A sharp decline in stocking activity in the third quarter of this year

to 0.5 mill barrels per day from 1.2 mill barrels per day in the second

quarter suggests that we might see a significant decrease in the

inventory build-up by China in 2018, Drewry concluded.

In the products trades, Asia’s front-month regrade (a measure of jet

fuel’s relative strength to gasoil) recently eased from last Thursday’s

19-month high of $1.58 per barrel but remained relatively strong at

$1.32 per barrel, Ocean Freight Exchange (OFE) reported.

While the surge in the Asian regrade can be partly attributed to

seasonality during the winter heating oil demand season, the bulk of

support is coming from the ongoing slump in the gasoil market.

Regional refineries have been running hard on the back of robust

refinery margins, as well as the end of turnaround season, flooding the

market with excess supplies. Unusually high diesel exports from India,

despite the end of monsoon season, have added length to an

already-pressured market, OFE said.

The jump in Indian gasoil exports can be attributed to Indian Oil’s

300,000 barrels per day Paradip refinery running at full capacity, as

well as the ramp-up of BPCL’s 310,000 Kochi refinery and HMEL’s 230,000

barrels per day Bathinda refinery after recent expansions.

Sentiment in the Asian high sulfur gasoil market weakened further after

the release of a new batch of Chinese export quotas, as well as China’s

domestic ban on diesel with sulfur content greater than 10 ppm, which

are likely to result in higher exports of high sulfur diesel.

The increase in cargo demand is reflected in the firm North Asian MR

segment. Rates for a South Korea/Singapore trip basis 40,000 are

currently assessed at $460,000, some 13% higher than at the start of the

month.

An increasingly narrow gasoil EFS and relatively high freight rates

have closed the arbitrage window to Europe, leaving Singapore as one of

the few viable outlets for excess barrels.

As such, onshore middle distillate inventories in Singapore stood at

11.55 mill barrels for the week ending November 9, up by 9.7%

month-on-month, OFE concluded.

Elsewhere, TEN has taken delivery of the Ice Class Aframax ‘Bergen TS’,

the last in the 15-vessel pre-employed newbuilding programme.

The ship was built by Daewoo-Mangalia and started a long-term charter immediately after its delivery.

The fleet expansion resulted in a 30% increase of TEN’s fleet over the last 18 months.

The first ship from the tranche, the 300,000 dwt VLCC ‘Ulysses’ was

delivered in May, 2016. She was followed by nine Aframaxes, two LR1s, a

DP2 Shuttle tanker, another VLCC and an LNGC.

With 65 vessels fully operational, TEN’s minimum revenue backlog comes

to 1.3 bill with average contract duration of 2.5 years, the company

claimed.

“With the largest growth in the company’s history, successfully and

timely completed, TEN is well positioned to take advantage of market

opportunities as they will appear,” Nikolas Tsakos, TEN President &

CEO, said. “The fully employed renewal programme is expected to

significantly contribute to TEN’s bottom line and solidify the fleet’s

income visibility and cash generation from now and into the future.”

In the charter market, the 2012-built VLCC ‘Trikwong Venture’ was

believed fixed to Koch for $27,500 per day, while the 2012-built Suezmax

‘Decathlon’ was taken by Total for 12 months at $19,000 per day.

In the Aframax sector, the 2006/07-built ‘NS Captain’ and ‘NS Columbus’

were thought fixed to Clearlake for 12, option 12 months at $15,500 per

day each. Vitol was said to have taken their near sister, the

2003-built ‘Petrozavodsk’ for six months at a similar rate. PBF Energy

was said to have taken the 1998-built ‘Eagle Austin’ for 12 months at

$15,000 per day and the 2004-built sisters, ‘Adafura’ and ‘Ashahda’ were

reportedly fixed to undisclosed interests for $14,500 per day each.

The recently delivered LR1 ‘Cielo Blanco’ was reported as fixed to

Trafigura for six, option six months at $13,750 per day, while Navig8

was believed to have taken the 2004-built ‘Theodosia’ for 12, option 12

months at $11,750 per day.

In the MR sector, Golden Stena Weco was thought to have fixed the

2017-built ‘Altair’ for two years at $15,000 per day, while Chevron was

said to have taken the 2009-built sisters ‘Nave Orbit’ and ‘Nave

Equator’ for 12, option 12 months at $13,500 per day.

ST Shipping was very active.This charterer was believed to have fixed

the 2005-built MR ‘Kriti Emerald’ for 12 months at $16,000 per day, the

2004-built ‘Jasmine Express’ for 12 months at $12,750 per day, plus the

2008-built Handysize ‘Hector N’ for 12 months for $12,000 per day.

In the S&P market, brokers said that the 2003-built Aframax

‘Singapore Voyager’ had been committed to Greek interests for $9 mill,

while Indian buyers were said to have committed $9.8 mill for the

1998-built Suezmax ‘Cap Georges’.

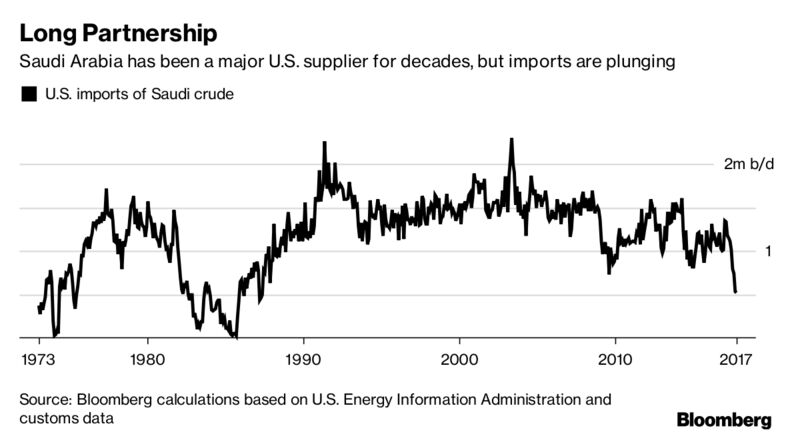

For a generation, the huge, whitewashed storage tanks at America’s

largest oil refinery in Port Arthur, Texas, have stored almost nothing

but Saudi crude.

The

plant is owned by Saudi Arabia’s state-run oil company, Aramco, and

since it first bought a stake in 1988, the Motiva refinery guaranteed

the kingdom a strategic foothold in the world’s largest energy market.

The tankers carrying millions of barrels a month of Arab Light crude

from Saudi export terminals to Port Arthur were testament to the

strength of the energy and political ties binding Riyadh and Washington.

All

of a sudden, there are very few Saudi ships arriving in Texas. Since

July, Aramco has constricted supply, attempting to drain the crude

storage tanks at Motiva -- and many others across America -- part of a

plan to lift oil prices, even at the cost of sacrificing its once prized

U.S. market.

While Motiva is most affected, the rest of the U.S. oil

refining system, from El Segundo in California to Lake Lake Charles in

Louisiana, has also taken a hit. The result: Saudi crude exports into

America fell to a 30-year low last month.

"The

drop is huge," said Amrita Sen, chief oil analyst at consultant Energy

Aspects Ltd. in London. "It’s not just that Saudi exports are low, but

they have been low for several months.”

At

a stroke, the freedom from Saudi oil that’s been a rhetorical

aspiration for generations of American politicians, from Jimmy Carter to

George W. Bush, is within reach -- even if it’s largely the choice of

supplier rather than customer.

The U.S. imported just 525,000

barrels a day of Saudi crude in October, the lowest since May 1987 and

down from 1.5 million barrels a day a decade ago, according to Bloomberg

News calculations based on custom data.

The export drop was part

of a wider undertaking by the Organization of Petroleum Exporting

Countries to fight a global glut that has weighed on oil prices. OPEC

and its non-OPEC allies including Russia are scheduled to meet later

this month to discuss prolonging the cuts through 2018.

Saudi

Arabia, which for decades fought hard to be the second-largest oil

supplier to the U.S. after Canada, last month dropped to fourth position

for the first time since at least 1990, falling behind Iraq and Mexico.

The

drop in supplies has been so dramatic that Motiva bought in July almost

exactly the same amount of crude from Saudi Arabia (4.01 million

barrels) as it did from Iraq (3.96 million), according to custom data.

Saudi crude that month accounted for just 36 percent of Motiva’s

imports, down from a typical 70-90 percent in the past.In August, the

most recent monthly data available at company level, Saudi crude

accounted for less than half of Motiva’s imports.

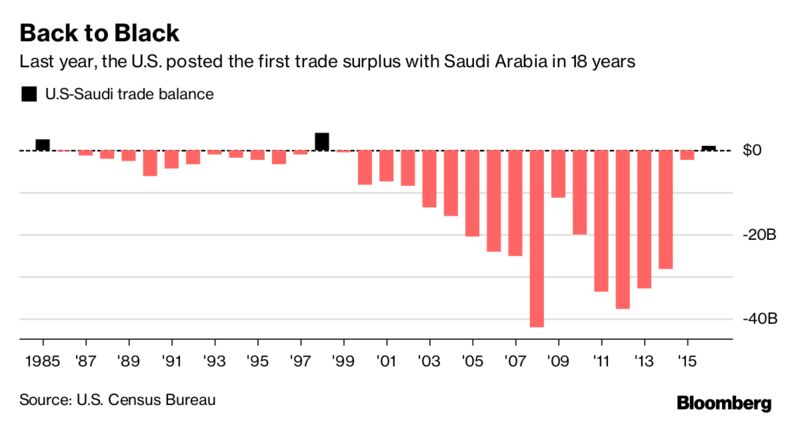

The combination

of falling Saudi oil exports into the U.S. last year, cheap crude and

higher exports of American weapons had already turned upside-down the

trade relationship between the two countries. Last year, the U.S.

enjoyed its first trade surplus with Saudi Arabia since 1998 -- only the

third in 30 years, according to data from the U.S. Census Bureau. The

sharper cuts in oil exports since the summer will likely amplify that

trend.

As

Saudi supplies fell, U.S. crude inventories dropped sharply over the

summer and autumn to their lowest since January 2016. Oil prices have

followed and Brent, the global benchmark, traded at a two-year high

above $60 a barrel this month.

"The policy has been a tremendous

success," said Anas Alhajji, a Dallas-based oil consultant who tracks

Saudi oil policy. "The U.S. is the only country in the world that

publishes oil inventories data on a weekly basis and investors closely

follow it. Saudi Arabia needed to focus on the data that matters to

investors, and it did by lowering exports to the U.S."

Saudi

officials said that oil exports are set to drop even further in this

month and next, with shipments into the U.S. expected to fall another 10

percent from November.

"The cuts show that when the Saudis say

they will do ’whatever it takes’ they mean it," said Helima Croft,

global head of commodity strategy at RBC Capital Markets LLC and a

former analyst at the Central Intelligence Agency.

Yet, driving

its exports into the U.S. to a three-decade low isn’t without risks for

Riyadh. Once a country gives up its market share, it can be costly to

recover it. The drop in Saudi shipments also reflects the changing U.S.

energy market as rising shale production reduces the overall need for

foreign oil. The EIA expects U.S. output to reach an all-time high of

10.1 million barrels a day by December 2018.

"Our import

dependence has collapsed," said Bob NcNally, a former White House oil

official and head of consultant Rapidan Energy Group LLC. "What should

worry Riyadh is if they need to sustain the cuts not a few more months,

but a lot longer.”

The International Energy Agency painted a rosy outlook

for U.S. domestic production up to 2025 in its annual World Energy

Outlook flagship report, saying the surge in oil and gas output in

America is the biggest boom in history.

However, owning Motiva gives Saudi Arabia a route to regaining market share, traders and refining executives said.

"Motiva

has taken the brunt of the Saudi cuts, so Riyadh would be able to

increase exports to the U.S. relatively easily in the future as and when

they decide to reverse the policy," said Sen at Energy Aspects.

For

the Saudi Arabian Oil Co., as Aramco is formally known, the loss of

market share comes at a delicate moment. The company is preparing for an

initial public offering that Riyadh hopes will value the company at an

eye-watering $2 trillion.

The

American market has long been Aramco’s most prized, and the Port Arthur

refinery is one of the company’s jewels -- nearly $10 billion was spent

expanding its capacity in 2013. In preparation of its initial public

offering, scheduled for the second half of 2018, Aramco earlier this

year paid to $2.2 billion to take full control of Motiva, dissolving a

50-50 joint-venture it held with Royal Dutch Shell Plc.

Aramco declined to comment.

At

any other time, the loss of U.S. market share would have worried the

Saudi regime, fearing a loss in political influence. But with President

Donald Trump, the Saudis believe the strength of their relationship with

the White House is as good as it’s been in decades, said David Goldwyn,

a Washington-based energy consultant and former U.S. State Department

top oil diplomat.

"The Saudis are not worried about the need to have U.S. oil market share to secure themselves diplomatically," Goldwyn said.

The

shift away from the U.S. show the increasing important of Asian markets

for Saudi Arabia, most notably China, but also India, Indonesia, Japan

and South Korea. While Saudi exports to the U.S. plunged, sales in Japan

earlier this year jumped to a 28-year high.

"Saudi Arabia doesn’t

care any more about its market share in the U.S -- it’s going after the

Asian market," said Jan Stuart, an oil economist at consultant

Cornerstone Macro LLC in New York.

The government of Ghana and US supermajor ExxonMobil are in talks

aimed at allowing the US firm to launch an exploration program off the

West African country’s coast.

In 2015 ExxonMobil and Ghana signed a

MoU to assess its Deepwater Cape Three Point region, where the water

depths range up to 13,000 ft.

The country’s deputy oil minister,

Mohamed Amin Adam, was quoted in a Reuters report as saying that the

government chose direct negotiation with the US firm over a competitive

tendering process due to the peculiar nature of the oilfield.

The

block was relinquished twice by Vanco Energy and Lukoil and that has

since increased its risk profile, according to the Ministry. A release

from the Ministry described the block as “one of the ultra-deep water

blocks, which severely tests the limits of modern technology and would

take research and development to optionally develop and exploit any

discovered resources.”

Gunvor

USA LLC, a subsidiary of Gunvor Group, has successfully closed the

syndication of its USD 875 million Borrowing Base Credit Facility.

The facility will support the company’s established

operations in the United States, as well as planned expansion into

Canada. Gunvor USA LLC has two main offices, located in Houston (TX) and

Stamford (CT), which are focused on trading refined products, crude oil

and natural gas.

“Our expanded facility enables Gunvor USA to build on our trading activities across the commodities space in North America,” said Chris Morran, Treasurer of Gunvor USA. “The

oversubscription of the transaction and 75% increase in the facility

amount demonstrate the level of confidence our banking partners have

with our North American strategy.”

The new facility is jointly lead arranged by Rabobank,

which will also serve as Administrative Agent and Active Bookrunner,

and ABN Amro Capital USA LLC as Joint Bookrunner. ING Capital, LLC,

Natixis, New York Branch, and Société Générale join as Joint Lead

Arranger in the transaction.

The syndicate also includes Credit Agricole Corporate and Investment

Bank, Deutsche Bank AG, New York Branch, Mizuho Ltd. and Sumitomo Mitsui

Banking Corporation.

“Gunvor USA has grown rapidly since its launch in 2016, and has significantly expanded its bank group as part of the refinancing,” said David Garza, President of Gunvor USA and Managing Director for its North American operations. “In

the last year, Gunvor USA has hired more than 60 people for its North

American operations, and opened trading offices in Houston and Stamford,

and now a rep office in Calgary. We’ve been able to grow at an

accelerated pace with the support of our banking partners.”

Gunvor USA LLC is a wholly-owned indirect subsidiary of Gunvor Group

Ltd., one of the largest independent energy commodity traders in the

world.

We may never fully know what lies behind Crown Prince Mohammed

bin Salman's decision to arrest more than 200 Saudi citizens, including

11 princes and four government ministers, on corruption charges, just

as tensions with Iran are escalating.

What we do know is that his

move simultaneously boosted the oil price and undermined the

attractiveness of Aramco to potential foreign investors. But it would be

a mistake to conclude that this political decision also heralds a shift

in Saudi oil policy, or permanently damages the prospects of the state

oil company's IPO.

Crude prices always rise in response to unrest

in the Middle East, even when the countries involved produce little or

no oil. That it has done so now, in the wake of the arrests in the

region's biggest producer and the threats against Lebanon and Iran in

response to a missile launched from Yemen, should come as no surprise.

The

jump, which took oil prices to their highest level in more than two

years immediately after the arrests, might be expected to boost support

for a pause before OPEC and its friends decide whether to extend their

current deal on production cuts until the end of 2018. There are some,

including Russian President Vladimir Putin, who have said that it is too

early to decide what should be done beyond the deal's current expiry in

March.

But dissenting voices are likely to fade into the

background when the groups meet in Vienna on Nov. 30. The output cuts do

not target a specific oil price -- as Saudi oil minister Khalid

Al-Falih said in June, the aim is to reduce excess inventories. That

problem has not yet been resolved.

MbS,

as the crown prince is widely known, is already setting the kingdom's

oil policy. He turned on its head Saudi Arabia's earlier stance of

boosting oil supply in an attempt to drive out higher-cost producers,

and he has placed his country at the forefront of output cuts aimed at

draining excess inventories, cutting production by more than required

under the agreement. He has already expressed support for extending the

production deal. Only by returning global oil inventories to more normal

levels can Saudi Arabia, and OPEC, hope to return to a world where

their actions influence the market.

The Saudi anti-corruption

purge should change nothing for the kingdom's oil policy. MbS is surely

mindful that an extension of the current output deal has already been

priced into the market, and failure to deliver it at the end of the

month would kill the recent rally in prices, despite the elevated

tensions in the Middle East.

Assessing the impact of the

detentions on the Saudi Aramco IPO is less straightforward. Ninety-five

percent of the shares will remain the property of what is now clearly an

unpredictable government. If the arrests turn out to be no more than a

purge of opponents to the crown prince's accession to the throne,

potential investors will run for cover.

But perhaps the anti-corruption purge is

the first step towards creating a more open and dynamic business

environment in Saudi Arabia. If it truly marks the beginning of the end

of the of the rentier state that has crippled the country's development

then it could even improve the prospects for inward investment, and

boost the attractiveness of the shares.

Foreign investors'

appetite for a piece of a partially-privatized Saudi Aramco will not

depend on whether the price of oil at the time of listing is $50, $60,

or $70 a barrel. A decision to invest in the company will depend much

more on the dividend and taxation policies of the major shareholder --

the Saudi government -- and the investor's view of the long-term future

for oil.

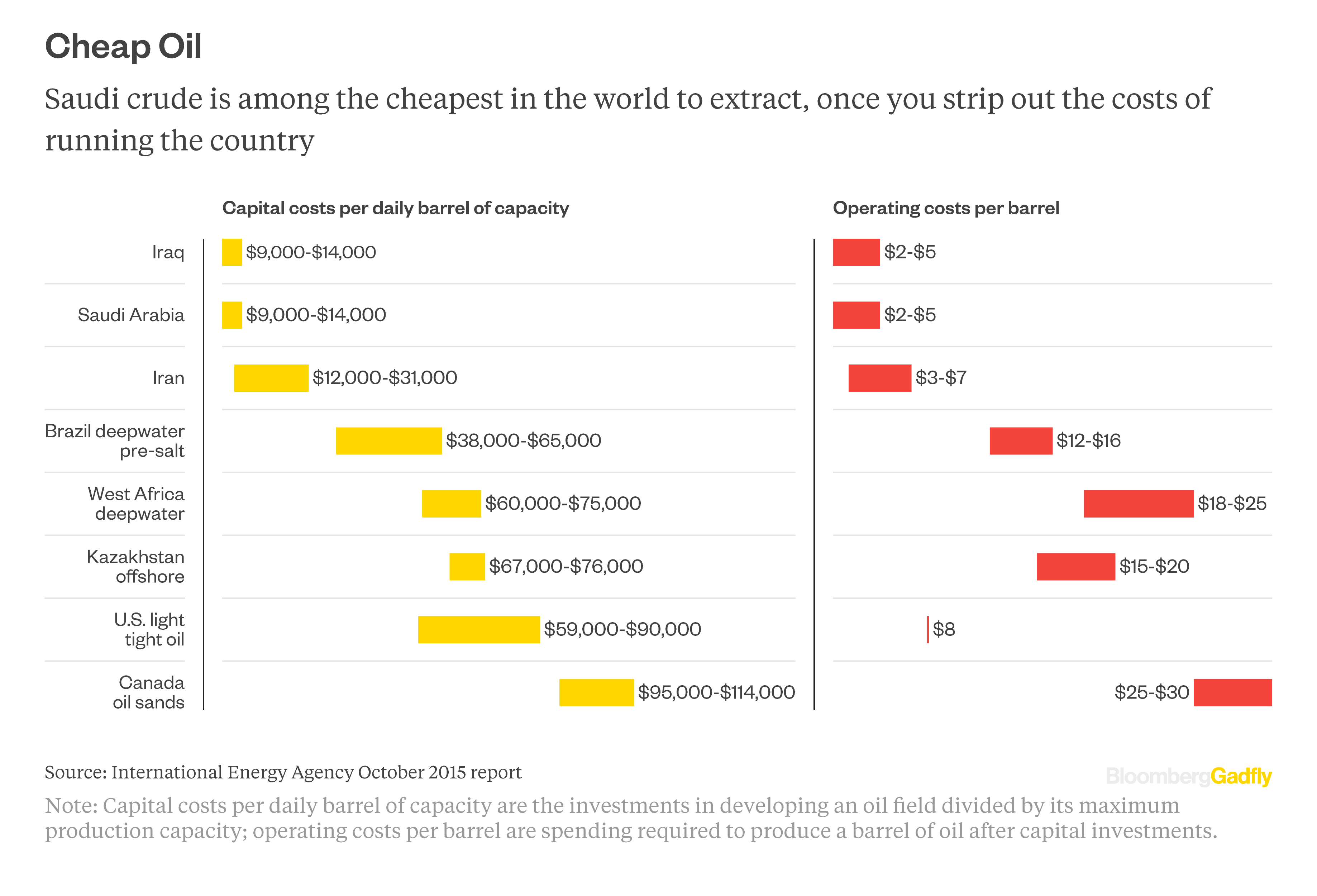

Indeed, it could be argued that over the longer term Aramco would benefit from a lower oil

price, which simultaneously boosts demand for crude and makes

alternative energy sources less attractive while undermining other,

higher-cost oil supplies. That ought to give the best outlook for

production as Aramco still extracts some of the lowest cost oil on the

planet. If Saudi Arabia's "Vision 2030" plan to wean the kingdom off its

dependence on oil revenues is even partly realized, Aramco will be

relieved of much of its burden of supporting government expenditure.

That should serve to burnish the appeal of the shares.

To realize

his dream of privatizing Aramco -- and the planned 5 percent offering

may be only the beginning -- the young crown prince will need to show

hoped-for investors that his recent purge of the kingdom's elite really

is a first step on the road to a brave new Saudi Arabia.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

The VLCC market remained flat during the past week for modern tonnage, as charterers focused more on older units.

These older vessels tended to be ex drydock with no SIRE, etc, which

were willing to accept a tempting rebate of some WS12-15 points for east

voyages, Fearnleys said in its weekly report.

The rebate closed in as the week progressed and increased resistance

from owners was seen. Looking ahead, owners’ sentiment remained strong

as the remaining 3rd decade cargoes were being worked. Delays were still

evident in the Far East, which added further pressure.

The Suezmax market also came under pressure over the past week.

Activity in West Africa slowed to a trickle and naturally the tonnage

list grew allowing charterers to chip away at levels from the early

WS100s down to the low WS80s.

The Black Sea and Med weather delays were minimal and again cargo

activity was been scarce allowing TD6 to fall sharply to WS90.

Current market conditions are bucking the normal 4Q17 more healthy

market trend and owners are running out of time with December dates

rapidly approaching. It is going to take a large volume of cargoes to

soak up the current tonnage back log, Fearnleys said.

However, a higher oil price is pushing up the bunker costs, which in

turn is eroding earnings. This could be the brake to stop further rate

slippage ahead.

Aframaxes trading in the North Sea and Baltic experienced an ongoing

decrease in rates this week. Less cargo activity, coupled with an

oversupply of available tonnage, gave charterers the upper hand and an

opportunity to push down rates.

Going forward, we see an even further downside before the market will firm again.

Last week, owners in the Med and Black Sea were holding out for high

numbers. But as the market fundamentals pointed towards a softer market,

the only thing keeping rates at such high levels was owners’

persistence.

By the start of this week, owners realised the list of available

tonnage was too long to play hard to get, and caved in one at the time.

The market has now dropped WS40 points and we could see it going below

WS100 by the end of this week, Fearnleys concluded.

The recent Iraq/Kurdish conflict heralds the return of the geopolitical

risk premium in oil prices, Ocean Freight Exchange (OFE) reported.

While the ongoing rally in crude prices is underpinned by fundamentals,

such as robust demand growth, ongoing OPEC supply cuts and falling US

crude inventories, growing tensions in the Middle East have been playing

an increasingly significant role.

With Iraq seizing control of the disputed Kirkuk region on 16th

October, Brent crude futures jumped to a three-week high of $57.82 per

barrel, as production at two major oilfields was shut. According to

Bloomberg, Kurdish crude exports fell by around 300,000 barrels per day

in October, due to supply disruptions.

Spurred by the sudden and unexpected purge in Saudi Arabia, oil prices

surged to their highest in two and a half years, as Brent crude futures

crossed the $64 per barrel mark on Monday.

The anti-corruption crackdown is viewed by many as a move by Crown

Prince Mohammed bin Salman to further consolidate his power at home, as

he pushes through major reforms, such as ‘Vision 2030’, which includes

the Saudi Aramco IPO.

Concerns over potential instability in the Kingdom and investment climate have added a geopolitical risk premium to oil prices.

If anything, the Saudi purge can be viewed as bullish for oil prices as

it further cements Saudi Arabia’s commitment to reduce the global glut.

Crown Prince Mohammed bin Salman has made his stance on extending the

ongoing OPEC cuts of 1.8 mill barrels per day clear, as higher oil

prices would benefit the IPO, OFE said.

The rollover of the OPEC production curbs for the whole of 2018 is

likely to further delay any significant recovery in the tanker market,

which is already facing headwinds from persistent overcapacity.

Lower cargo volumes ex-AG have contributed to the drop in average VLCC

earnings this year, which are currently around 40% less than that of

2016. The backwardated market structure has also led to the ongoing

decline in VLCC floating storage, which has released more tonnage into

the trading fleet, OFE concluded.

Meanwhile, the 2006-built MR ‘Pretty Scene’ is due to be publicly auctioned at Durban, South Africa on 5th December this year.

Bowman Gilfillan is handling the auction, which has materialised as a result of a judicial arrest.

Monjasa has confirmed that it is to charter an SKS Tankers Holding ‘D’ class Aframax.

The 119,000-dwt tanker will form part of Monjasa’s operations covering

West Africa, which comprises 15 tankers delivering a total of 1.5 mill

tonnes of marine fuel anually.

Several advanced technical features and the ability to load, discharge

and blend multiple grades of cargo simultaneously, made this vessel an

interesting proposition, the company said.

Group CEO, Anders Østergaard, explained:“It’s a pioneering move to

apply an SKS D-class tanker as a floating storage and this first-class

vessel becomes the largest ever member of Monjasa’s fleet.

"The aim is to strengthen the backbone of our West Africa logistics and

offer more flexibility for our customers taking bunkers in the region.

For this purpose, we see her as an excellent solution for current and

future trading requirements,” he said.

The vessel has six double valve segregations and is equipped with Framo deepwell cargo pumps for each individual tank.

Monjasa will take delivery of the vessel in Europe, and she will be fully operational off West Africa during December, 2017.

In other chartering news, Koch was said to have fixed the 2011-built

VLCCs ‘Maersk Heiwa’ and ‘Mercury Hope’ for two years at $29,000 per

vessel.

The 2007-built Aframax ‘Bai Lu Zhou’ was believed taken by Trafigurafor

12 months at $13,500 per day, while ST Shipping was thought to have

taken the 2009-2010-built sister Aframaxes ‘SN Claudia’ and ‘SN Olivia’

for 12 months at $15,500 per day.

Petrobras was said to have chartered the 2005-built MR ‘Aris’ for 30 months at $14,350 per day.

In the S&P sector, Greek interests were said to have taken the

newbuilding Suezmax ‘RS Aurora’ for an undisclosed fee, while Aegean was

thought to have bought the 1999-built Aframax ‘Althea’, which brokers

said was an old sale.

Central Shipping was believed to have ordered one, option one MR at

Hyundai Mipo for a reported $32-$35 mill per ship and delivery in 2019.

JEDDAH: Saudi Arabia has uncovered corruption to the tune of $100 billion.

In a statement on Thursday, Attorney General Saud Al-Mojeb said: “The

investigations of the Supreme Anti-Corruption Committee are proceeding

quickly ... The potential scale of corrupt practices which have been

uncovered is very large.”

Based on the investigations over the past three years, Al-Mojeb

estimated that “at least $100 billion has been misused through

systematic corruption and embezzlement over several decades.”

He said a total of 208 individuals have been called in for questioning

so far. Of them, “seven have been released without charge.”

Al-Mojeb, who is also the member of the anti-corruption committee, said

the evidence for “this wrongdoing is very strong and confirms the

original suspicions which led the Saudi authorities to begin the

investigation into these suspects in the first place.”

He said given the scale of the allegations, the Saudi authorities, under

the direction of the Royal Order issued on Nov. 4, had a clear legal

mandate to move to the next phase of “our investigations, and to take

action to suspend personal bank accounts.”

“On Tuesday, the governor of the Saudi Arabian Monetary Authority (SAMA)

agreed to my request to suspend the personal bank accounts of persons

of interests in the investigation,” he said.

Al-Mojeb admitted that there has been a great deal of speculation around

the world regarding the identities of the individuals concerned and the

details of the charges against them.

“In order to ensure that the individuals continue to enjoy the full

legal rights afforded to them under Saudi law, we will not be revealing

any more personal details at this time,” he said.

“We ask that their privacy is respected while they continue to be subject to our judicial process.”

He reiterated that it was important to repeat, as all Saudi authorities

have done over the past few days, that normal commercial activity in the

Kingdom is not affected by these investigations.

“Only personal bank accounts have been suspended. Companies and banks are free to continue with transactions as usual,” he said.

Al-Mojeb said: “The Government of Saudi Arabia, under the leadership of

King Salman and Crown Prince Mohammed bin Salman, is working within a

clear legal and institutional framework to maintain transparency and

integrity in the market.”

Saudi Crown Prince Mohammad bin Salman’s unexpected crackdown has shattered the tranquility of the kingdom.

After

Saturday’s news emerged that a long list of high-profile Saudi royals,

military leaders and multi-billionaires were arrested or confined to

their quarters, all seemed to be only an implementation of the crown

prince’s open threat that “no-one is above the law, whether it is a prince or a minister.”

The

current list of arrests include names like Saudi billionaire Prince

Al-Waleed bin Talal, one of the most media-loved Saudi businessmen, and

Prince Miteb bin Abdullah, former head of the Saudi National Guard. At

the end of the weekend, the impact was clear: The new Saudi power broker

isn’t cutting anyone slack.

Just after that, in an effort to

clean house in one fell swoop, Mohammad bin Salman (MBS) announced—by

royal decree—a new anti-corruption committee.

At the moment, most

eyes are on the anti-corruption narrative, which is being pushed by the

Saudi government and media. The announcement of the arrests, made over

Al Arabiya, the Saudi-owned satellite (whose broadcasts are controlled

by the state), showed MBS’s willingness to address corruption. Clearly,

corruption and a lack of transparency is still a significant issue in

Saudi Arabia, and MBS is taking a risk in challenging it.

It seems

the crown prince is far from finished, as news has emerged that one of

the Arab world’s leading broadcasters, MBC, has been put under

government control. Part of its management was removed and the owner

detained. News is also emerging that even the former Saudi Minister of

Oil Ali Al Naimi, Saudi Arabia’s media face for decades, has been

forcibly confined to his quarters.

Other

sources state that a travel ban has been imposed for Saudi officials,

including some figures within Saudi Aramco. The latter have been

informed that travel requests are currently on hold. More interesting is

that the Saudi Monetary Agency (SAMA) has ordered a freezing of

accounts of individuals linked to corruption. SAMA reiterated the

respective accounts of companies have currently not been frozen.

Regarding

the Saudi royals, most princes and princesses are currently prohibited

to travel, except with the permission of King Salman. Foreign money

transfer also has currently been limited to $50,000 per month, with a

two-month limit. Security sources indicate that Saudi princes in Tabuk,

Eastern Province and Mecca have been put under house arrest. At the

same time, Saudi special forces have moved to surround the residencies

of Prince Mishal bin AbdulAziz, Prince AbdulAziz bin Fahd and Prince

Khalid bin Sultan.

These developments are going further than the

original anti-corruption crackdown. The already long-foreseen power

struggle to take the Saudi throne seems to be entering its second phase.

Crown Prince bin Salman seems—supported by signs of support coming from

Washington, Moscow and even Arab neighbors—to take the chance to

overwhelm his local opponents by shockwave tactics. Some indicate that

they expect a possible change of guard at the top in the next couple of

days.

Each day’s developments grow more significant. MBS was able

to increase his own position dramatically this weekend, and continues to

remove remaining opposition by the dozen.

Although short-term

volatility could occur, overall stability and change inside of the

kingdom is to be expected, as MBS and his supporters are holding not

only the military and security forces in their hands, but have also

gained the trust and support of the majority of the Saudis.

MBS

has the same charisma as John F. Kennedy had when took the U.S.

presidential office. The crown prince has gained an almost movie-star

popularity under the young Saudis, who form the majority of the

population.

These current developments didn’t come out of nowhere.

The basis for the anti-corruption crackdown was supported by the

success of the Future Investment Initiative 2017. Dubbed “Davos in the

Desert”, this high-profile gathering of the world’s leading financial

power brokers happened in Riyadh last week.

At the event, MBS

received the green light to pursue his Saudi Vision 2030 dream to wean

the kingdom from its hydrocarbon addiction. In the same week, U.S.

president Trump and his administration increased their support for the

Saudi hardline position to Iran, IRGC and Hezbollah. Washington also

increased its pressure on Qatar to soon move away from Tehran.

These

regional and geopolitical developments have bolstered the views of the

MBS to pursue his strategy of confronting Iran and its proxies. It’s no

coincidence that the start of the crackdown popped up at the same time

that Lebanese prime minister Hariri took refuge in the kingdom. Thus,

the link with Hezbollah-Iran and Lebanon isn’t difficult.

Without

trying to assess the present situation as dire and threatening, all

signs show that the region, under influence of Saudi’s new de-facto

ruler, is heading toward a full confrontation with Iran. The internal

Game of Thrones of Saudi royals is now being slowly but obviously

transformed to a full-scale showdown with Iran and its proxies.

Saudi

Arabia—supported by the UAE, Bahrain and likely Egypt—was openly given

the green light by Trump’s secretary of treasury and secretary of state.

The silence on the Russian front indicates a possible change of heart

in Putin’s coterie, as well. Saudi Arabia and others openly stated that

Iran has committed several acts of war against the kingdom. The

ballistic missile attack by Houthi rebels on the airport of Riyadh is

directly linked to an act of war by Iran, perceived to be the provider

of these systems.

The coming days are crucial for the region’s

stability and future. The ongoing power struggle in the kingdom, which

is currently openly on the streets, not only targets corruption, but is a

move to consolidate power by Crown Prince bin Salman. His movement is

clear, and should perhaps be supported in full, as it could lead the

change that young Saudis want. The outcome will decide the further steps

needed by all parties involved.

Considering the signs, the most

positive outcome would be a consolidation of the position of MBS as the

main power broker, leading to a full implementation of Saudi Vision

2030. In the short term, this won’t prohibit the Saudis and their allies

to react and act with full military power against the Iranian power

projections and its proxies in Yemen, Lebanon and Iraq.

Stability

and security in Saudi Arabia is seen as a leading factor in MBS’s power

strategies. Confrontations inside and outside the kingdom aren’t seen as

a no-go area. After decades of listening to U.S., European or Russian

advice, MBS is creating his own future. Short-term financial or economic

instability and geopolitical risks have increased substantially in the

last 24 hours.