Oyu Tolgoi open pit has been producing since 2012. (Image courtesy of Turquoise Hill.)

https://www.mining.com/web/copper-mine-flashes-warning-of-huge-crisis-for-world-supply/

Accompanied by tinny taped music and overall-clad workers, Rio Tinto Group executives and Mongolian officials gathered a kilometer beneath the freezing Gobi Desert earlier this year to open one of the world’s richest underground copper mines.

Oyu Tolgoi, in southern Mongolia just north of the Chinese border, is key to Rio’s efforts to move beyond its dependence on iron ore and expand in copper, the metal that underpins the clean energy transition. It’s also a vast deposit whose corporate, political and technical vicissitudes offer a glimpse of the red metal’s troubled future.

As demand for copper surges, supply is increasingly likely to come from mines like this one on the arid steppe: expensive, technically complex, outside traditional copper jurisdictions and operating under the eye of governments jealously guarding their natural resources.

“There’s a huge crisis,” says Doug Kirwin, one of the earliest geologists to work at the deposit that became Oyu Tolgoi, or Turquoise Hill, named after the area’s rocks, stained by oxidized copper.

“There’s no way we can supply the amount of copper in the next 10 years to drive the energy transition and carbon zero. It’s not going to happen,” adds Kirwin, now an independent consulting geologist. “There’s just not enough copper deposits being found or developed.”

Analysts at Wood Mackenzie estimate a greener world will be short about six million tons of copper by next decade, meaning 12 new Oyu Tolgois need to come online within that period.

But they aren’t — there are simply not enough new mines, much less enough large ones. The result is a gap: BloombergNEF estimates appetite for refined copper will grow by 53% by 2040, but mine supply will climb only 16%.

The world’s largest miners aren’t standing idly by. After more than a decade of repenting for the excess that followed the China-led boom in demand in the 2000s, deals are back, with green metals in buyers’ sights. The looming green metal shortfall has encouraged Glencore Plc’s move on Teck Resources Ltd, long a coveted copper target, and top gold miner Newmont Corp’s record bid for Australian peer Newcrest Mining Ltd, a deal that will add bullion but also copper to its production profile. BHP Group Ltd has just completed the acquisition of copper producer Oz Minerals, its largest deal in over a decade.

None of these, even if successful, will alter the overall global balance.

Building mines, as opposed to buying them, is still too painful a headache. Prices are not shiny enough to cover rising costs, and risks abound. Take Oyu Tolgoi, where construction has involved adding a 200km labyrinth of concrete tunnels to the open pit, but also roads, an airport, power transmission and water infrastructure. Never mind Mongolia’s largest canteen, for 20,000 or so workers — and, Mongolia hopes, an eventual power plant.

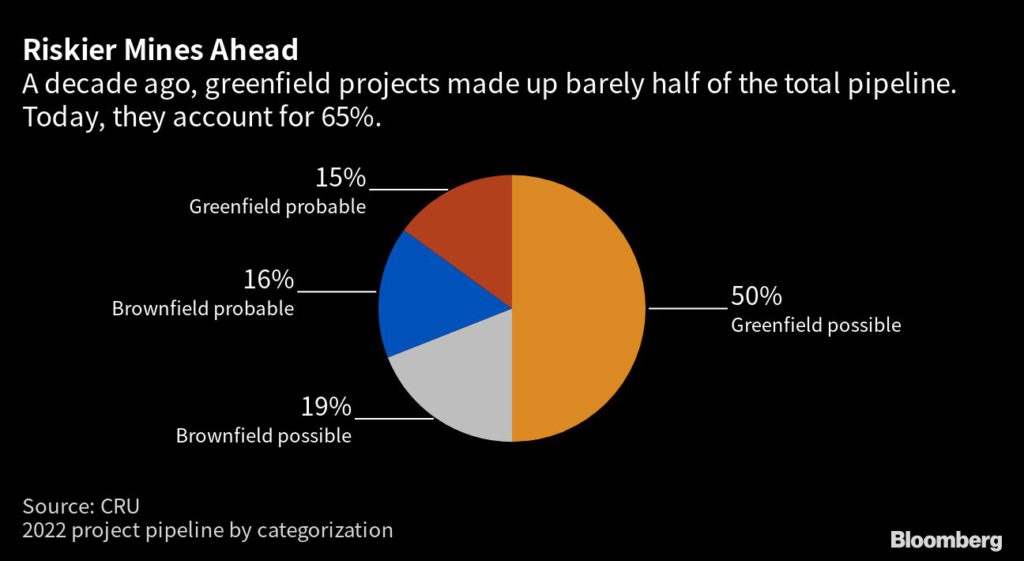

Even more worrying, though exploration has ticked higher of late, is that spending remains far short of what is required. And what does emerge tends to be smaller and lower grade, meaning the percentage of metal in the ore is more slight, so more effort (and waste) is required to hit the same production levels. The last heavyweight discovery, aarguably, was roughly a decade ago — the combined Kamoa-Kakula operation in the Democratic Republic of Congo, owned by entrepreneur Robert Friedland’s Ivanhoe Mines.

“Mines are getting older, mines are getting deeper, and mines are getting lower grade,” said David Radclyffe, managing director at Global Mining Research. “Then you’ve had the added complications of the need to conform with the shift in terms of environmental requirements. And political risk on top of that.”

Geologist Kirwin’s skepticism comes from deep experience. It was his team that, more than two decades ago, discovered the mega-deposit that eventually lured Rio to Mongolia.

Hunting for copper in Asia for Friedland, he arrived in Ulaanbaatar in 1996, after a chance encounter in China with a Mongolian geologist. Mongolia had barely emerged from its communist past as a Soviet satellite state. It was, as he had been promised, a geologist’s paradise, offering tantalizing prospects — including around Oyu Tolgoi in the south, where outcrops had first been spotted in the mid-1980s.

Magma Copper, later bought by mining giant BHP, had started exploring in the Gobi desert in the mid-1990s. When the miner decided to refocus, Kirwin was there to secure the exploration license for Oyu Tolgoi. Friedland describes the moment as a “perfect storm”. He moved fast, and drilling soon yielded one of the world’s largest high-grade copper discoveries.

The scale of the find — plus unrelenting promotion from the expansive Friedland, who had made his name with the giant Voisey’s Bay nickel deposit in the 1990s — brought attention, and in 2006, Rio Tinto took a stake in Friedland’s company.

“There was no doubt that it was exactly the sort of project that Rio Tinto goes after – tier one, large size, long life, low operating cost. So that was the basis of their interest,” says David Paterson, who became Rio’s country director for Mongolia in 2010.

But the path was not smooth. There was boardroom trouble, as Rio began increasing its holding and Friedland sought to prevent it gaining control with a poison pill takeover defense — one which the Anglo-Australian miner eventually defeated. Friedland, who takes credit for the open pit and the first phase of the mine, left with a hefty payout.

There was turbulence too with the Mongolian government, as the mine hit local headlines. A deal that granted the country a 34% stake in the mine — with payment, plus interest, to be taken from future profits – began to seem less generous as the expansion hit delays, pushing back the expected windfall.

The result was so messy and the financing so tricky that a resolution in 2015 helped the then-head of copper, Jean-Sebastien Jacques, make it to chief executive the following year. And setbacks continued as late as 2019, when technical challenges meant costs for the underground mine escalated to more than $7 billion — a third more than initially planned.

“Both sides were playing the card that they would walk away,” said Paterson, who by that time had left Rio and was watching from afar. “I never believed that.” The dispute eventually resolved when Rio agreed in December 2021 to write off the Mongolian government’s debt to the company, to the tune of $2.4 billion.

When Rio chief executive officer Jakob Stausholm and Mongolian Prime Minister Oyun Erdene Luvsannamsrai stood side by side under the Gobi desert in March, neither was able to ignore the past, but neither dwelled on it.

Bold Baatar, Rio’s Mongolian-born head of copper and long the man at the sharp end of negotiations, brushes aside fresh political concerns today: “There’s a lot of openness about how the government works with the broader society,” he said, speaking at Oyu Tolgoi’s airport after the underground mine ceremony.

But even democracies can have disagreements on critical issues, from the fiscal burden to water use and waste. “I do believe that there will be debate in the future too,” Oyun Erdene told Bloomberg in an interview.

Other issues loom. The Mongolian government wants Rio to build a power plant for the mine, rather than use electricity from over the border, generated in China. It is also eager for copper to be smelted at home rather than sent out on trucks — an idea that would be expensive and water intensive, and for which Rio has shown little enthusiasm.

These demands will be familiar to all major miners, as countries attempt to create more value within their borders, to protect resources and increase fiscal benefits, from Chile, rethinking tax demands to meet acute social spending needs, to Panama, where a spat with the government forced First Quantum Minerals Ltd’s Cobre Panama mine to a halt.

But that’s not all. Oyu Tolgoi is also emblematic of the growing technical challenges for miners. Even historic open pits like century-old giant Chuquicamata, the Chilean mine that drove revolutionary icon Ernesto Che Guevara to action, are going underground.

Oyu Tolgoi, which Rio forecasts will be the world’s fourth-largest copper mine when it is at full production, uses a complex method that allows access to deeper deposits called “block caving”, which involves digging under the ore body, blowing gaps underneath that allows the ore to collapse and fall down funnels to a lower level where it is collected, crushed, and sent to the surface on conveyor belts.

A cost-effective way of mining large deposits less rich than those of the past, its popularity is spreading, but the technique remains a challenge. Rio found early on that its ore collapsed all too well. Then there’s the hefty initial investment.

“You can almost count the number of miners who can do that on one hand,” said veteran analyst Glyn Lawcock at Sydney-based investment firm Barrenjoey, who first visited Oyu Tolgoi on Friedland’s private jet.

Rio’s Baatar is bullish. He argues disputes over “mega-mining contracts” are common, and doesn’t think Rio’s experience over Oyu Tolgoi was particularly unusual. Nor does he think political instability elsewhere will hold back copper supply.

But his optimism is not widespread.

Take not just Chile, with its revisions to fiscal policies for miners, but Peru, a country long considered crucial to the next wave of copper production, where the mining sector has been battered during lengthy social unrest. Rio in late March agreed to sell a controlling stake in its Peruvian mine La Granja to First Quantum.

“What the market never predicted was how difficult South America would become,” said Radclyffe. “The uncertainty out of both Chile and now ongoing in Peru, that’s just added an extra level of complexity that the market never expected, and that hasn’t really been resolved.”

The problem now is that the next big deposits will require possibly more risk than most executives at the helm of large miners are willing to take. Even before that, it requires a significant increase in exploration spending.

“It’s similar to what you saw in the 90s. There was huge underinvestment in 90s, a lot of money went into the tech boom 1.0 — then you had China urbanization, this big demand shock that the industry wasn’t prepared for,” said John Stover, a portfolio manager at Tribeca Investment Partners in Singapore. “Everyone knows what’s happening, but we’re not seeing the spending.”

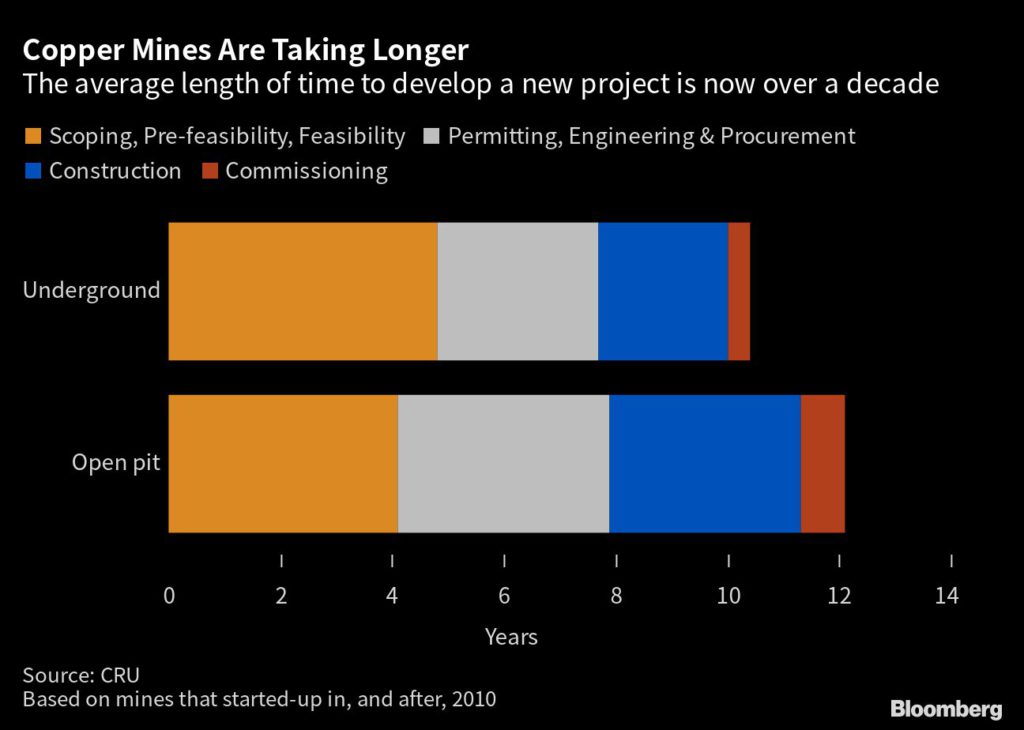

Friedland, still one of the mining industry’s most committed boosters, agrees — and warns that the sheer length of time involved in bringing on new mines can rarely be shortened, even when exploration money is spent and a deposit found.

“Oyu Tolgoi is now 20 years old, and it’s just getting started,” he said. “It doesn’t matter whether the copper price is $3 a pound or $30 a pound, you can’t speed up the process materially.”

Granted, there are other options — recycling, or new methods to extract copper from lower grade ore and even mine waste. BHP, Rio and others have bet on cutting-edge technology. But in the face of rocketing demand, none will move the needle.

“If it was rolled out across every operation in the world, it could be another half a million tons added on,” said Wood Mackenzie analyst Carl Firmen — who estimates the annual supply gap will be 12 times that figure by next decade.

Other, more futuristic methods, such as use of underground robots and microbes to get more out of low-grade or hard-to-access deposits are at an even earlier stage.

Rio, of course, hopes to be among the beneficiaries whatever happens, with rising demand pushing prices higher just as copper output at Oyu Tolgoi reaches peak production. At that point, the company projects, it will be up there with the giants.

Greening the economy, expanding grids and renewable energy generation to hit global climate targets, however, requires many more Oyu Tolgois.

“Mongolia was an adventurous location. So was the Democratic Republic of Congo,” says Friedland. “But this has to be done. Absent this effort, there is absolutely no chance of an energy transition. It’s a fantasy.”

(By James Fernyhough)

No comments:

Post a Comment