Cargo ships entering one busiest ports in Singapore. Stock image.

Doug King set up his hedge fund in the early days of the commodity super-cycle in 2004. It was perfectly timed: voracious Chinese demand lifted the price of everything from oil to copper to record highs. Investors flooded the commodities sector. At the peak, King’s Merchant Commodity Fund was managing about $2 billion.

“We are facing a structural inflation shock,” King said. “There’s a lot of pent up demand, and everyone wants everything now, right now.”

For the first time since the pre-crisis years before 2008, the commodities boom means central banks are fretting about inflation. The rally will have a political impact, too. With oil back at $75 a barrel, Saudi Arabia and Russia are back in the driving seat of the global energy market — a remarkable come back from negative prices just over a year ago. The boom is also an unwelcome development for policymakers tackling the climate crisis: rising commodities prices will make the shift more expensive.

China, reliant on raw materials imports to feed millions of factories and building sites, is so nervous the government has tried to force prices lower, threatening crackdowns on speculators and releasing strategic stockpiles. It’s worked to some extent — copper has given up all its gains this year— but prices across the complex remain robust: iron ore is still near a record, U.S. steel prices have tripled this year, coal has risen to a 13-year high and natural gas prices are on a tear.

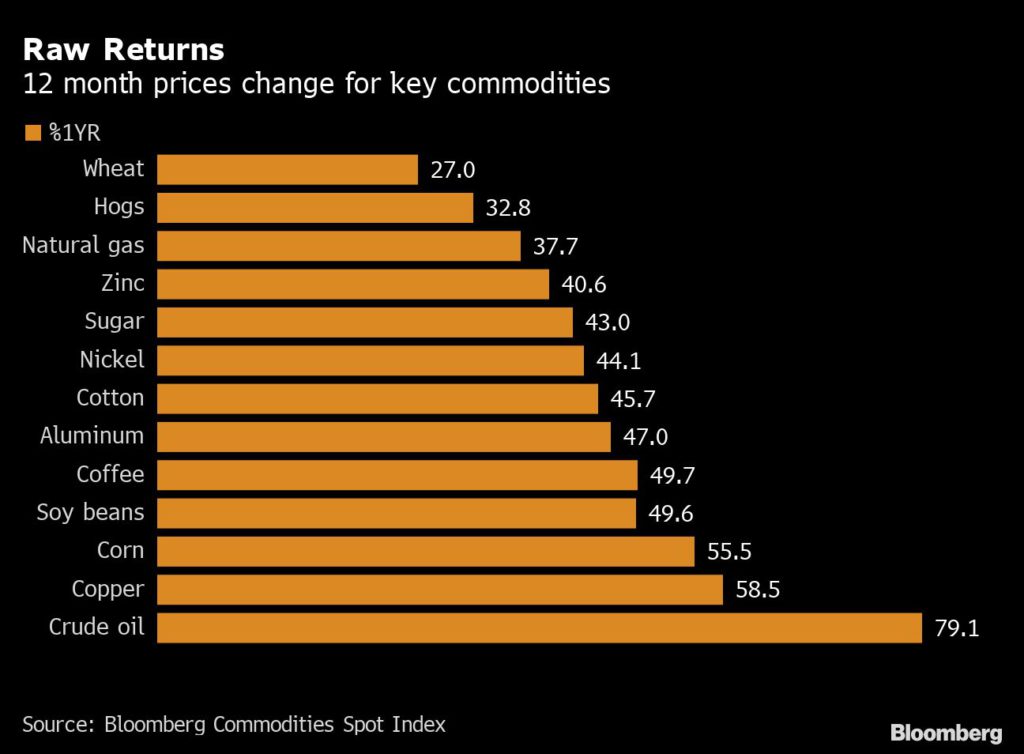

Even after the recent pullback, the Bloomberg Commodities Spot Index, a measure of 22 raw material prices, is up 78% from the March 2020 low when the pandemic first hit.

And crude oil, the global economy’s most crucial commodity, keeps powering higher as the world emerges from lockdown and the OPEC+ alliance puts a lid on supply. Benchmark Brent prices are up 45% this year, prompting traders and Wall Street banks to talk again about the potential for prices to surpass $100 a barrel for the first time since 2014.

As prices have surged, so has Wall Street’s interest. The annual Robin Hood investor conference, which every year congregates hedge fund luminaries from Paul Tudor Jones to Stanley F. Druckenmiller and Ray Dalio, featured a panel on commodities earlier in June — the first time in at least five years the conference has found time to discuss raw materials.

Jeff Currie, Goldman Sachs Group Inc.’s veteran head of commodities research, who argues for a long-term bull market across commodities despite the recent sell-off in metals and grain, says there’s room for a lot more investment into the market.

“Commodities are back in vogue,” Currie said, but so far the excitement about sky-high prices hasn’t yet attracted the money flows the sector harnessed during the 2004-2011 boom.

For those investors and physical traders who have already poured cash into commodities, betting on post-pandemic recovery, the rally has showered them in money.

Take Cargill Inc. The world’s largest trader of agricultural commodities made more money in just the first nine months of its fiscal year than in any full year in its history as net income surged above $4 billion.

Or Trafigura Group, the world’s second biggest independent oil trader, where the more than $2 billion in net profit posted in the in six months to the end of March was nearly as much as it made during its previous best ever full year.

“Our core trading divisions are firing on all cylinders,” said Jeremy Weir, the chief executive of Trafigura.

For consumers, however, the commodity boom means rekindling memories of high inflation. For now, companies are mainly absorbing the brunt of the impact, pushing factory inflation in some countries, including China, to their highest in more than a decade. But sooner or later, consumers will pay the price, too.

From Unilever Plc to Procter & Gamble Co., companies have announced plans to raise prices in the near term.

“We’re seeing levels of commodity inflation that we have not seen in a very long time,” Graeme Pitkethly, the chief financial officer at Unilever, told investors after disclosing first quarter results. “The commodity inflation that we’re seeing is impacting all businesses.”

he speed and breadth of the rally, affecting dozens of raw materials from vegetable oil to coal, have prompted many to talk about a new commodities supercycle, similar to the one that started nearly two decades ago as China’s rapid industrialization changed the structure of the global economy.

Economists typically define a supercycle as a period of abnormally strong demand that oil companies, miners and farmers struggle to match, sparking a rally that outlasts a normal business cycle. Before China, modern history century witnessed three distinct commodities supercycles, each driven by a transformational socioeconomic event. U.S. industrialization sparked the first in the early 1900s, global rearmament fueled another in the 1930s, and the reconstruction of Europe and Japan following World War II powered a third during the 1950s and 1960s.

The emergence of a fifth supercycle would be a major event. The price rally backs the talk of a new boom: the Bloomberg Commodity Spot Index, a basket of 23 raw materials, is nearly 500 points, matching the 2007-08 and 2010-11 peaks. And yet, what’s more likely happening is that the world is still experiencing the impact of the China-led supercycle, now turbo-charged by counterintuitive economic shifts triggered by the coronavirus pandemic.

Initially, Covid was bad news for commodity demand. The world went into lockdown, travel plunged and factories closed. The price of everything from oil to copper followed consumption, falling sharply between March and May of last year. But after the first few months, the world started to get back on its feet and consumption patterns changed in a way that favored commodities.

To appreciate what happened, the key is understanding the typical relationship between commodity demand and wealth. Generally, poor countries consume few raw materials because most spending is devoted to basic needs, like food and shelter.

The sweet spot for commodities is countries with per capita income between $4,000 and $18,000 — the middle-income range that China entered in the early 2000s. It translates disproportionately into commodity demand because it’s at the level when countries urbanize and industrialize. At those per capita income ranges, families have money to buy cars, household appliances and other goods that require lots of raw materials. Industrializing countries also build railways, highways, hospitals and other public infrastructure.

Above $20,000 per capita, demand for commodities starts to cool down as richer populations devote incremental wealth to services like better education, health and recreation.

The coronavirus pandemic altered those dynamics. With many families under lockdown, spending shifted from services into goods everywhere, even in the richest nations like the U.S. In many ways, American and European consumers behaved for a few months like their counterparts in emerging countries, spending on everything from new bicycles to television screens.

The U.S. economy offers the best example of the trend. Overall consumer spending remains below the 2018-19 trend, but that masks a huge divergence between spending in goods and services. According to the Peterson Institute for International Economics, household spending in goods is now running 11% above the pre-pandemic trend; meanwhile spending in services, like holiday, restaurants or entertainment, remains 7% below the pre-pandemic trend.

“Ultra-accommodative monetary policy, unprecedented fiscal stimulus, pent-up demand, strong household balance sheets, and record savings all combine to paint a picture of a resilient and strong growth trajectory,” said Saad Rahim, chief economist at Trafigura. The fiscal stimulus has other parallels with emerging markets as Western governments are targeting infrastructure spending, promising to rehabilitate their highways, railways and bridges.

Governments are also keen to build a greener future, spending on electrification to move away from fossil fuels. While that’s bad news for coal and oil, it means more demand for raw materials like copper, aluminum and battery metals like cobalt and lithium that are key for the energy transition.

“Commodity prices will stay strong for a long way longer,” said Ivan Glasenberg, the outgoing CEO of commodities giant Glencore Plc. For the first time the world’s two super powers, the U.S. and China, were simultaneously pushing big infrastructure projects as a way to rescue their economies from the impact of the coronavirus pandemic, he said.

Supply is struggling to catch up. Some of the bottlenecks are due to deliberate moves by producing countries, like the OPEC+ alliance, which slashed oil production last year. And others are due to the difficulty of running mines, smelters, slaughters houses and farms in the middle of the pandemic.

Crucially for the longevity of the rally, there’s a structural supply constraint that means high prices may not work as a signal to increase production and eventually bring the market back into balance.

The forces slowing the supply response are twofold. First, companies are under pressure from shareholders and courts to join the fight against climate change, reducing their production of fossil fuels like coal, oil and gas. Second, the same shareholders are demanding that chief executives reward them with higher dividends, in turn leaving less money to expand mines or drill new wells.

The impact of those forces are evident already in some corners of the commodity market, where companies stopped investing in new supply several years ago. Take thermal coal, for example. Mining companies have been cutting spending since at least 2015. As demand has picked up, coal prices have jumped to levels unseen in 10 years. The same has happened in iron ore, where prices shot up to all-time high earlier this year. Next is likely to be oil, where companies are cutting spending significantly.

For the commodity bulls, like Doug King, the hedge fund manager, it’s the sign to double down. “This is the beginning of a proper boom cycle — this isn’t a transitory spike,” he said.

(By Javier Blas)

No comments:

Post a Comment