https://www.mining.com/copper-production-to-show-strong-and-consistent-growth-for-next-decade/

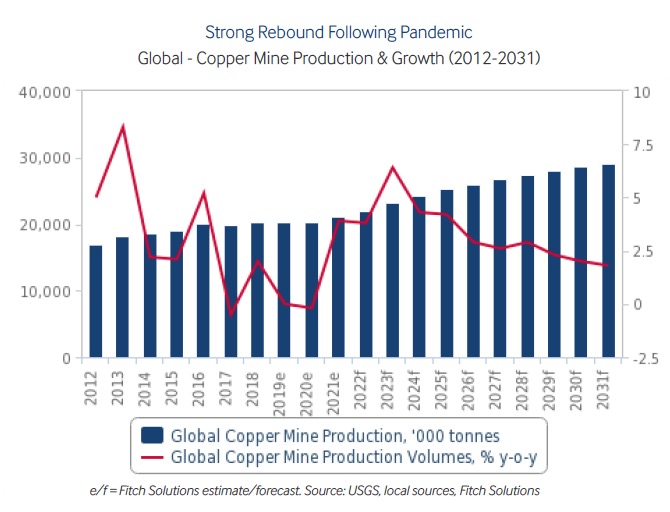

A new study by Fitch Solutions Country Risk and Industry Research forecasts 7.3 million tonnes will be added to global copper production through 2031 as a raft of projects in Chile, China and Congo come online.

Chile

The market researcher says top producer Chile will show a slight decline in the short term due to ongoing drought affecting mines such as Anglo American’s Los Bronces and Antofagasta’s Los Pelambres operations, labour action at state-owned Codelco and unforeseen maintenance at Vale’s mines.

However, longer term the country, which is responsible for a quarter of global production, will experience strong growth led by large scale miners. BHP is adding substantially to Escondida’s output following the end of covid restrictions, Teck Resources’ Quebrada Blanca Phase 2 project is expected to complete construction around the end of 2022, while Codelco is undertaking a $1.6 billion project to overhaul its Salvadore mine and add 47 years to its mine life.

“Downside risks to long-term production stem from the possibility of a mining sector tax, which President Gabriel Boric is pursuing. Nevertheless, given significant opposition in Congress to the original proposals, we expect the impact on output to be limited,” says Fitch.

China

Fitch expects Chinese copper mine production growth to slow sharply from an average growth rate of 6.9% over the past decade to 1.0% through 2031 due to the shutdown of low grade mines and delayed capacity expansions.

Ramp ups at new projects, including Yunnan Copper’s Pulang mine and Zijin Mining’s Qulong complex will offset declines elsewhere.

Peru

Fitch expects Peruvian output growth to slow dramatically in the near term from its earlier estimates due to community protests affecting key mines including MMG’s Las Bambas and Southern Copper Corp’s Cuajone mines. The authors of the report do not anticipate that annual production will reach pre-covid levels until 2024.

China will play an increasingly important role in Peru’s copper sector, says Fitch, pointing to the country’s Ministry of Energy and Mines forecast of a total of $10.2 billion to be invested by Chinese firms in five mining projects over the next 10 years.

DRC

The Democratic Republic of the Congo, thanks mainly to Ivanhoe Mines and Zijin Mining’s giant Kamoa-Kakula mine expansion, will exceed annual production of 2 million tonnes for the first time next year and reach nearly 3 million tonnes in 2031.

Glencore’s restart of the Mutanda copper-cobalt mine and China Minmetals’ Deziwa project, held with state-owned Gecamines will further add to the central African nation’s strong growth.

Price slump

The copper price has been in retreat since hitting all-time highs in March and was last trading at $3.28 a pound ($7,230 a tonne) in New York, a 10-week low.

Fitch expects prices to average $8,400 a tonne in 2023 and $11,500 a tonne by 2031 as a long-term structural deficit emerges due to the very strong long-term demand outlook.

No comments:

Post a Comment