- Major oil and gas pipeline projects have faced regulatory and political roadblocks forcing them to halt production or cancel new development.

- The recent crude oil crash led to a steep reduction in U.S. rig count and as the shale boom contracted amid a weaker global economy, pipeline capacity was overbuilt.

- But even as climate change pressures

the fossil fuel industry, natural gas is not going away, say energy

experts, with gas making up 40% of power generation, growing LNG export

markets and more-friendly drilling regions in states like Louisiana and

Texas.

With the coronavirus pandemic slashing demand for the oil and gas that has been booming in the U.S. shale during the past decade, energy pipeline development has stalled. The midstream portion of the energy complex, as it is known, may not recover soon, but it will recover, according to energy experts, and none other than Warren Buffett — who has been uncharacteristically shy about making investments during the Covid-19 washout — is betting on that. The billionaire investor recently plunked down near-$10 billion to buy gas pipeline assets and related debt.

After a decade of capacity buildout in the pipeline infrastructure to match the U.S. fossil fuel fracking growth, demand is lacking and will stay down, despite a doubling in the price of crude following sub-$20 lows reached in March.

“The midstream is in a tough spot,” said Luke Jackson, senior analyst, natural gas, North America, S&P Global Platts. “You have to consider what drove the infrastructure development: the shale boom. When you look at oil near $40 and natural gas rising, but still sub-$3, we’re not in a climate where higher production of oil and gas is supported to support a larger build out,” Jackson said.

Before Covid-19 hit, Platts Analytics was forecasting U.S. crude oil production to rise by one million barrels per day year over year, and rise by another 600,000 barrels in 2021. Now, as rig counts have declined at the steepest rate since 2009 — 75% of natural gas production comes from the “associated gas” at oil rig sites, as well — crude production is expected to register an annual decline within the next few months, and that decline will persist until at least mid-2021, according to Platts Analytics’ forecast.

Instead of the substantial growth that midstream companies had been making investment decisions based on — and which led to a significant number of pipeline projects coming online within the past two years — major shale basins like the Permian will see lower utilization of outbound pipelines for the next few years.

Platts

“We’re not expecting U.S. crude to return to levels we were at in Q1 2020 until 2023,” said Jenna Delaney, lead analyst, North American oil, S&P Global Platts. “It will be even a few more years until we get back to where we started from, and then to satisfy pipeline capacity, we will need even more production growth.”

But there’s more going on then just a typical commodities boom-and-bust cycle. With successful environmental challenges leading to legal and regulatory roadblocks for pipelines, and a political climate becoming more difficult for fossil fuels, companies in the utility sectors are rethinking their midstream investments, and in some cases, reallocating funds towards renewable energy projects.

Earlier this summer, the Energy Transfer-owned Dakota Access Pipeline, which runs from North Dakota to Illinois storage facilities and the Gulf Coast, was forced by a federal judge to

shut down production pending further environmental impact reviews by

the Army Corps of Engineers. The halt in production resulted in a major

win for the Standing Rock Sioux Tribe, which has been fighting a legal

battle against the pipeline operating and transporting oil for nearly

three years.

“I’m not aware of a pipeline that’s been forced to shut down mid-production, that obviously concerns people in the industry,” said Pearce Hammond, managing director and equity research analyst for midstream and infrastructure at Simmons Energy. “It just shows how difficult it is to get a pipeline built in the U.S. because of regulation, environmental concerns, and with environmentalists pushing against it.”

Dominion Energy and Duke Energy announced the cancellation of the Atlantic Coast Pipeline due to “legal uncertainties” surrounding the project. The cost of the project had increased from nearly $5 billion to $8 billion, amid ongoing legal battles surrounding permits and environmental issues.

In a separate capitulation, last month Dominion sold its natural gas pipeline assets to Warren Buffett’s Berkshire Hathaway in $9.7 billion deal that included close to $5 billion in pipeline assets, as well as assumption of debt.

Why Buffett is bullish on gas

According to Steve Fleishman, managing director and utilities analyst at Wolfe Research, Buffett’s acquisition will provide a steady stream of revenue and a quality asset, regardless of the lack of midstream development. Buffett also has always preferred investments in a market where more control is reasonable to expect — lack of new pipeline supply could be a plus as far as his preference for less competition likely to come into the market. The Dominion gas pipeline and storage assets include operations in Connecticut, Maryland, Ohio, West Virginia, Pennsylvania, New York, Maryland and Virginia.

The deal won’t burn a hole in his pocket, either, with Berkshire sitting on well over $100 billion in cash and short-term assets, and Buffett always anxious to deploy the capital into projects that generate a return on investment.

It’s not just the political optics, though that plays into the shift highlighted by Dominion away from midstream. The market has been downgrading the value of gas pipeline assets owned by utilities. Even with one of the biggest utility operations in the U.S., Berkshire’s cash hoard can operate like a private equity buyer flush with cash., Stand-alone utilities, meanwhile, are increasingly focused on environmentally sensitive portfolios, according to Sophie Karp, KeyBanc Capital Markets utilities and renewables sector analyst.

“We’ve seen in the past year, even before Covid, that the premium commanded by gas assets evaporated,” Karp said. “The market was saying that it doesn’t want utilities to own gas assets.”

Morningstar analyst Gregg Warren projects that the Dominion pipeline assets will generate $1 billion in earnings before interest, taxes and depreciation and amortization, for Berkshire Hathaway Energy’s pipelines unit, which will see mid-single-digit EBITDA growth. The $9.7 billion deal was estimated at a price of 9.7 times EBITDA, a price that Dominion management defended as being above recent, similar transactions.

Assets like the ones Dominion sold to Berkshire are harder for utilities to justify given the push among constituents to decarbonize. “The incremental investor in utilities is more environmentally conscious than the incremental investor in Berkshire,” Karp said. Referring to sensitive bases of ratepayers in regions around the country where utilities are regulated and resistance to fossil fuels are growing. she added, “A suburb in Boston will not make or break a utility, but it could be a precursor to ‘a death by a thousand cuts,’ where each incremental rate case there is more severe opposition to capex that is not decarbonized.”

“It’s not ‘tomorrow we stop using gas,’ but it is a plausible scenario where it gets harder and harder for a utility to put dollars into that infrastructure and derive earnings growth,” Karp said.

The utilities’ market dynamic partially explains why Buffett was able to make the deal without paying a hefty premium. “It wasn’t the top of the market,” the KeyBanc analyst said. “It sold at the peer group average at a time when the average was down ... but Dominion was trying to rip the Band-aid off.”

Dominion is moving in another direction, with significant offshore wind opportunities in some of its markets, like Virginia.

“That may be more attractive than gas, and when can redirect the capex and get a return on that, and not deal with gas ownership, it looks like a solid move,” Karp said.

Dominion pointed to the “state-regulated nature” of its business profile as one of the reasons for the deal, as well as noting its net zero target by 2050 for both carbon and methane emissions, and $55 billion planned in next 15 years for emissions reduction technologies including zero-carbon generation and energy storage.

Utilities owning midstream gas assets outside their core business will be slowing down as a business focus, with the premiums formerly commanded no longer available. Utility stocks did well in recent years, but “the stocks have not done well on mistream deals,” Karp said. “The trend will be utilities looking at divesting, not investing more. ... But natural gas as a fuel is not going away in our lifetime. The long-term use case is there.”

Concerns about future oil and gas capacity

With declining access to domestic oil supply as midstream development cease, some analysts worry about the potential for energy security risks and the U.S. becoming again reliant on foreign exporters, such as OPEC.

Hammond at Simmons Energy said the recent regulatory hurdles in the oil and natural gas markets could ultimately mean, “you’d be relying on increasing very insecure sources of supply, which is something we’ve tried to move away from in terms of energy security, turning the clock back to the 70′s, 80′s.”

“The policy makers are trying to balance the transition to lower carbon and meet the needs now while still being energy secure,” he said.

“Certainly, if we see muted or no U.S. production growth, when demand continues to recover globally, we’re gonna have to be more reliant on foreign imports that we would have been, certainly seeing energy security issues,” said Leo Mariani, energy stock analyst at KeyBanc Capital Markets.

But in the mid-term, what is maybe more likely is a bifurcation in the U.S. pipeline market, as U.S. oil and gas production growth comes back, rather than a return to the OPEC-dictated era.

Platts expects U.S. production growth to start recovering for U.S. shale by 2023, and does not expect midstream constraints, especially as Canadian crude continues to flow into the U.S. and the export market for liquified natural gas continues to grow.

“We do believe that the U.S. will need more infrastructure development to support higher movement of gas to markets in the Gulf Coast, in East Texas and Louisiana,” Platts’ Jackson said.

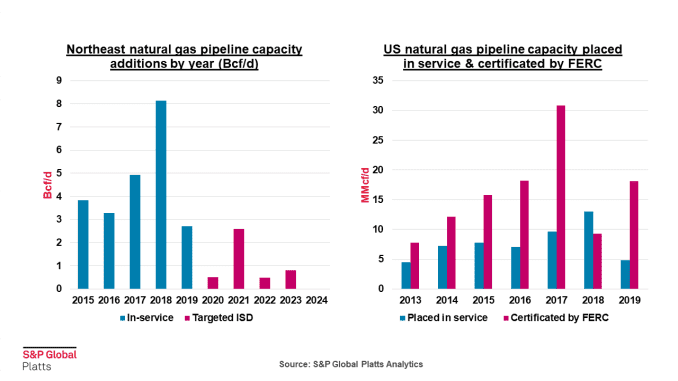

The situation in markets like the Northeast and its big population centers will be more challenging for building pipeline.

“It will be much easier to build pipelines in certain areas,” said Eric Brooks, Northeast US natural gas analyst, S&P Global Platts. “In the Northeast, it’s a more intense regulatory environment and that does come back to politics. Atlantic Coast Pipeline was emblematic and it is no secret it is challenging environment.”

Broader market shift to renewables

What is happening at Dominion is also occurring within the oil and gas industry. BP recently took a step that would have once been considered unthinkable when it reported a loss of $6.7 billion — the oil and gas giant halved the dividend that has long been coveted by pension fund investors and committed to a new strategy of increasing investments in renewable energy and cutting oil and gas generation by 40%.

Equinor, the Norwegian petroleum company formerly known as Statoil, also is transitioning its business model to include more renewable energy, including offshore wind projects as its primary way to accelerate a transition to low-carbon energy sources. The changes, though, are less than absolute: Equinor’s near-record breaking offshore wind project will provide renewable energy to oil and gas platforms.

“They can see clearly that something needs to be done about climate change,” said Andrew Grant, head of oil and gas for Carbon Tracker, a think tank that focuses on the financial and market implications of climate change. “An increasing numbers of countries around the world have set zero targets .... we’re going to need other alternatives and less fossil fuels, and companies understand that, and they want to build in some future-proofing ... to build out some of those energy sources. They’re stuck between that and the fact they have a very long history of producing oil and gas fields,” Grant said.

A report from Rystad Energy forecasts the global number of drilled oil wells to be at 55,350, the lowest number of wells since the early 2000s and a 23% decline in the number of wells drilled in 2019. Even further, North American drilling is expected to remain 50% lower than last year’s levels.

“A lot of pressure is coming through from all stakeholders, consumers, and civil society, but also investors, especially in the past few years. Investors realize there is a risk and they want to be reassured. It has become clear that oil and gas companies have underperformed in the market. Investors realize that the world is going to decarbonize,” Grant said.

For Dominion, the business model is changing more quickly.

“They made a decision to exit this midstream pipeline business because they basically felt that it [renewable energy] would be a better business, it would basically accelerate the transition of the company to clean energy, For them, it’s a pretty big strategic bet they made,” Fleishman said. “They’re making a bet the new model of the company will have better growth and better financial strength and more focus on clean energy will get a higher valuation.”

Even as he increases his pipelines footprint, Buffett’s utility has been making a considerable shift. It is already one of the biggest wind energy producers in the U.S. through its MidAmerican Energy utility affiliate based in Iowa, while its NV Energy in Nevada plans to increase its renewable generation to a percentage in the high 40s by 2023, mostly using geothermal and solar power.

Some make the case that the Buffett pipeline buy is about electric vehicles playing a bigger role in the future. But in a broader sense, Buffett has parted ways with a strict decarbonization investing philosophy in a core belief that he outlined to Berkshire shareholders who were concerned about climate change back in 2014. Buffett said that whether the investment decision was about Berkshire Hathaway or “virtually all the companies I can think of,” he didn’t believe that “climate change should be a factor in the decision-making process.”

—Additional reporting by Eric Rosenbaum

No comments:

Post a Comment