Since

the lifting of a decades-old ban on crude exports at the end of 2015,

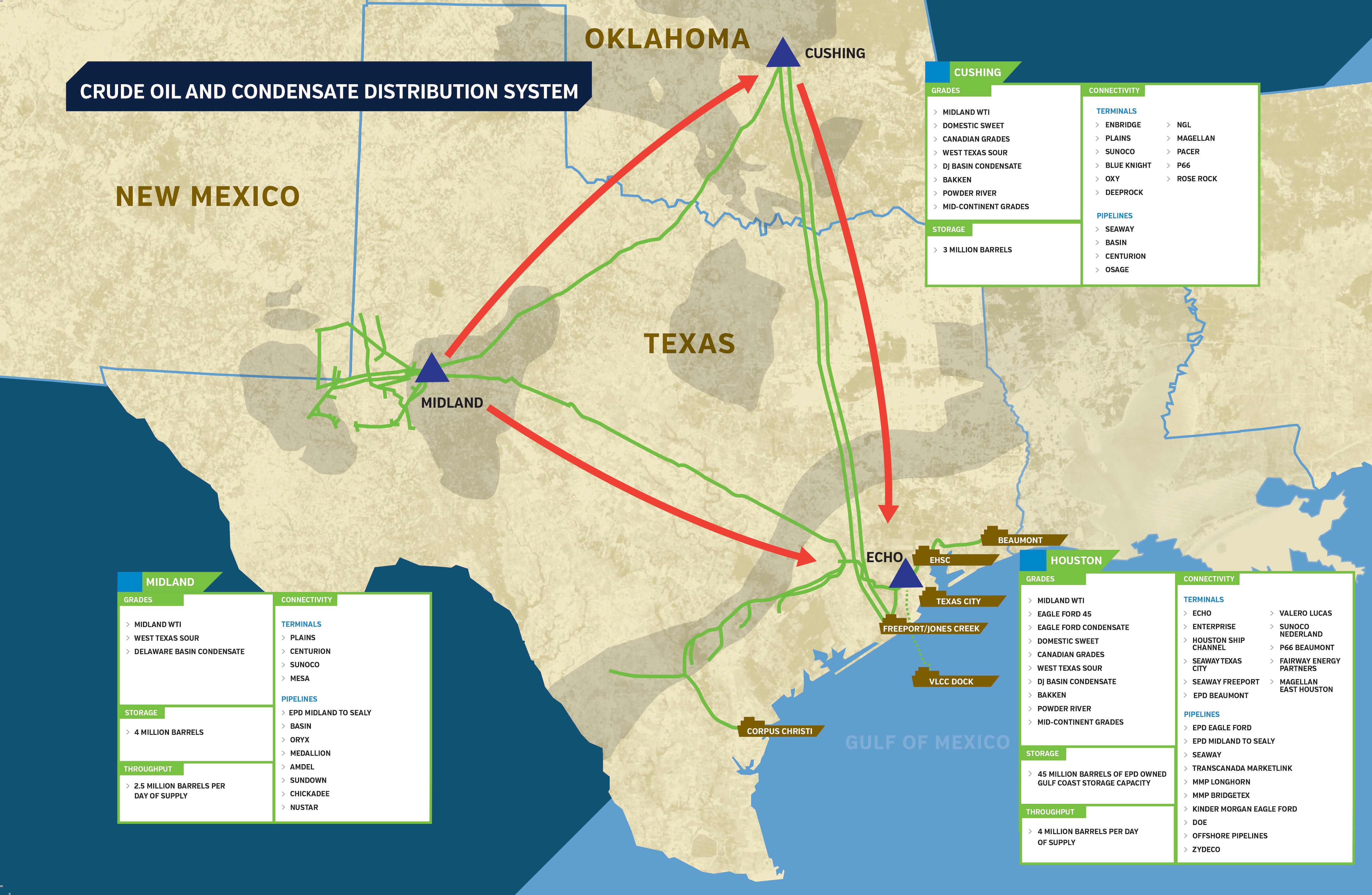

Houston has emerged as a major physical crude oil trading hub,

overtaking the country’s primary crude benchmark (West Texas

Intermediate, or “WTI”) pricing power long held in Cushing, Oklahoma due

to access to major pipelines that run through it and ample storage

space.

The surge in crude oil production can be tied to the shale boom,

particularly in the Permian Basin in West Texas and New Mexico, where

vast amounts of crude oil flow directly to the Gulf Coast – oftentimes

bypassing Cushing altogether – to destinations such as Asia, Europe and

Latin America.

Traders and market observers say WTI crude at Houston is a preferred

futures contract hub over WTI Cushing because it better reflects global

market balance and offers a more liquid market for export customers.

Since the lifting of the crude oil export ban, U.S. crude exports

have surged nearly 350%, from 490,000 barrels per day (bbl/d) in January

2016 to a record 2.2 MMbbl/d in June 2018, according to the U.S. Energy

Information Administration (EIA).

Rising oil production in the Permian Basin, which is estimated at

around 3.5 MMbbl/d, along with increased U.S. light sweet crude exports

to overseas customers, have prompted the launch of new physical futures

contracts in Houston that are set to debut later this year.

In fact, the U.S. port district of Houston-Galveston earlier this

year began exporting more crude oil than it imported for the first time

on record, according to EIA statistics. In April 2018, crude oil exports

from Houston-Galveston surpassed crude oil imports by 15,000 bbl/d. In

May 2018, the difference between crude oil exports and imports increased

substantially to 470,000 bbl/d.

On July 17, 2018, the Intercontinental Exchange Inc. (“ICE”)

announced plans to launch in the third quarter of this year a physically

delivered Permian WTI crude oil futures contract, deliverable in

Houston. According to ICE, the new futures contract “is designed to provide price discovery, settlement and delivery at Magellan Midstream Partners LP’s terminal in East Houston.”

The contract is expected to provide ample liquidity for traders and

brokers seeking flexible hedging and trading opportunities for export

shipments.

Meanwhile, CME Group on September 24, 2018, announced that it intends

to offer a new WTI Houston crude oil futures contract with three

physical delivery locations on the Enterprise Houston system, pending

regulatory review. WTI Houston crude oil futures will be listed with and

subject to the rules of NYMEX, beginning with the January 2019 contract

month.

The new WTI Houston crude oil futures contract expands CME Group’s

already robust suite of crude oil futures and options and will

complement its global benchmark NYMEX WTI Light Sweet Crude Oil futures.

Participants will have the flexibility to make or take delivery of U.S.

light sweet crude oil at the Enterprise Crude Houston (“ECHO”) terminal, Enterprise Houston Ship Channel (“EHSC”) or Genoa Junction through the new contract.

Enterprise has a network of 19 ship docks along the U.S. Gulf Coast

and is the largest exporter of crude oil in the U.S. and the ideal

provider of delivery points for this physical WTI Houston futures

contract, according to CME Group.

Through its network of pipelines, storage and marine terminals, the

firm has the capability to handle the flow of more than 4 MMbbl/d of

crude oil. Participants will also benefit from access to a diverse group

of refiners, storage facilities and export facilities through the

Enterprise network.

What We’re Hearing

Opportune LLP’s Derivative Valuation group has heard very little from

our existing clients about the new WTI Permian crude oil contracts

delivered into Houston. Unfortunately, this is very common as we often

deal with transactions that have already been executed.

That being said, we routinely see examples of hedging mismatches. For

instance, some companies have marketing agreements that sell WTI at

Cushing and are erroneously hedged with Brent crude contracts. These

pricing relationships tend to deteriorate over time and eventually

result in both losses on production and the hedge itself. These costly

mistakes can easily be avoided.

No comments:

Post a Comment